Picture supply: Getty Photographs

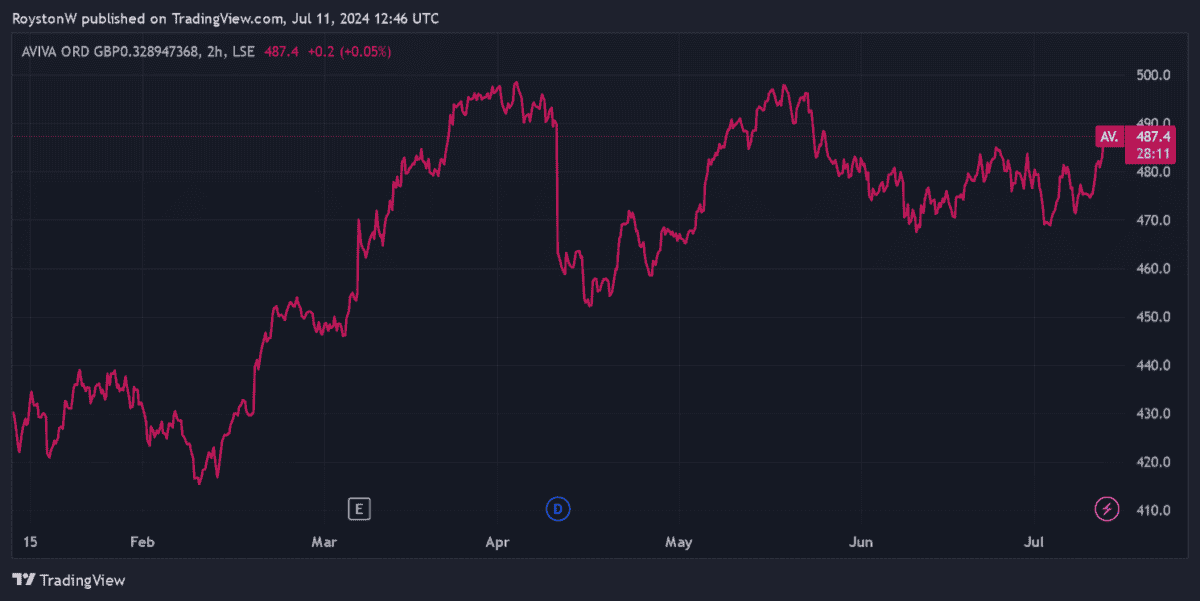

Aviva‘s (LSE:AV.) share value has soared in 2023. Up 12%, the monetary companies large has risen on improved hopes for the UK’s financial and political panorama. Predictions of rate of interest cuts from the summer time that might stimulate client spending has additionally boosted the worth.

But at 487.4p per share, I consider the FTSE 100 agency nonetheless seems dust low-cost. Listed here are a number of explanation why.

Earnings metrics

The very first thing to do is contemplate Aviva’s share value relative to predicted earnings. Primarily based on this, the corporate scores fairly nicely, in my opinion.

Metropolis analysts suppose the underside line will develop 20% yr on yr in 2024. This leaves Aviva buying and selling on a sexy price-to-earnings (P/E) ratio of 10.7 occasions.

Nevertheless, the Footsie agency’s price-to-earnings progress (PEG) ratio is much more spectacular. At 0.5, it’s beneath the watermark of 1 that signifies a inventory is undervalued.

The PEG ratio stays low at 0.8 for 2025 too, due to predictions of one other double-digit rise in annual earnings.

Dividend yields

The subsequent step is to try the dividend yield on Aviva shares. To offer some context, it’s a good suggestion to check how the corporate compares on this entrance towards the broader FTSE 100.

The agency’s dividends have recovered strongly because the pandemic, and Metropolis analysts count on this pattern to proceed. Consequently, the ahead dividend yield stands at an unlimited 7.1%, nearly double the three.6% Footsie common.

In additional excellent news, brokers suppose dividends will hold rising sharply over the subsequent two years as nicely. And so the yield marches to 7.8% and eight.4% for 2025 and 2026 respectively.

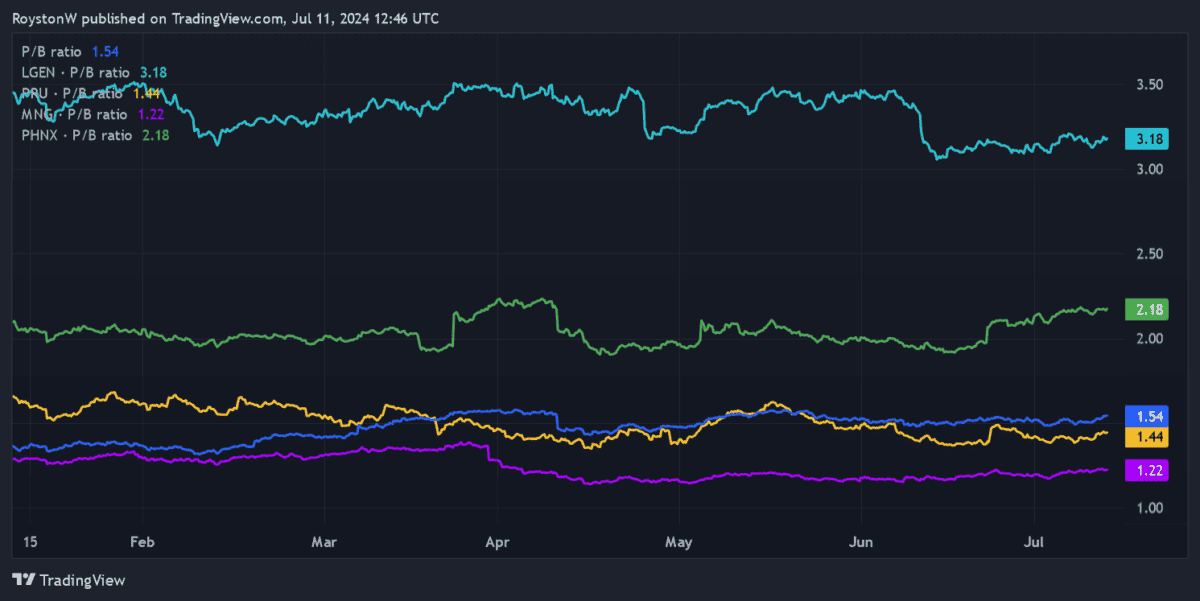

Guide worth

At face worth, Aviva’s share value doesn’t look so low-cost relative to the worth of its property. Proper now, the corporate trades on a price-to-book (P/B) worth of 1.4 occasions.

A studying above 1 signifies the market values a share extra extremely than the e-book worth of its property.

Because the graph above reveals, this studying is a long way beneath these of Authorized & Basic Group and Phoenix Group Holdings, however above these of Prudential and M&G.

Nevertheless, with the trade common coming in at 1.9 occasions, Aviva’s P/B worth really seems respectable at the moment.

A prime worth inventory

Lately Aviva has undertaken a sequence of huge disposals, the newest of which noticed it promote its Singapore Life division in March. This raises danger because it’s rather more depending on robust financial circumstances in a slender choice of nations (specifically the UK, Eire and Canada). As we all know, the UK economic system hasn’t been firing on all cylinders and UK customers haven’t felt massively assured of late.

But the corporate’s capability to develop earnings and dividends sooner or later stays good. Model energy makes it a market chief in lots of safety, retirement and insurance coverage product classes. And because the saving wants of a rising aged inhabitants enhance, it might be within the field seat to proceed rising gross sales quickly.

All issues thought-about, I believe it’s one of many FTSE 100’s most tasty worth shares proper now.

{kind=link}