Picture supply: Getty Photographs

I’m on the lookout for the very best dividend shares to purchase for a four-figure passive earnings in 2025. However I’m not simply concentrating on short-term returns. I’m looking for firms that might pay a big and rising dividend earnings over time.

Listed below are two from the FTSE 100 and FTSE 250 on my radar right now:

| FTSE 100/FTSE 250 inventory | 2025 dividend per share (f) | Dividend yield |

|---|---|---|

| Rio Tinto (LSE:RIO) | 310.4p | 6.5% |

| Grocery store Revenue REIT (LSE:SUPR) | 6.13p | 8.2% |

If forecasts are appropriate, a £20,000 lump sum funding unfold equally throughout these shares will present £1,480 value of dividends in 2025 alone.

Right here’s why I’d purchase them for my portfolio if I had money to take a position right now.

Rio Tinto

Rio Tinto’s a share I already maintain in my Shares and Shares ISA. And following latest heavy share worth weak spot I’m contemplating rising my stake.

In addition to boasting that vast 6.5% dividend yield, the mega miner additionally now trades on a low price-to-earnings (P/E) ratio of 8.9 occasions.

Income are in peril as China’s financial system — which gobbles up swathes of the planet’s uncooked supplies — experiences as prolonged stoop. However I believe the cheapness of Rio Tinto’s shares at present displays this risk.

I definitely consider earnings right here will rise strongly over the long run as commodities demand booms. This can be pushed by themes like the expansion of synthetic intelligence (AI), the renewable power increase, and ongoing urbanisation and infrastructure spending throughout the globe.

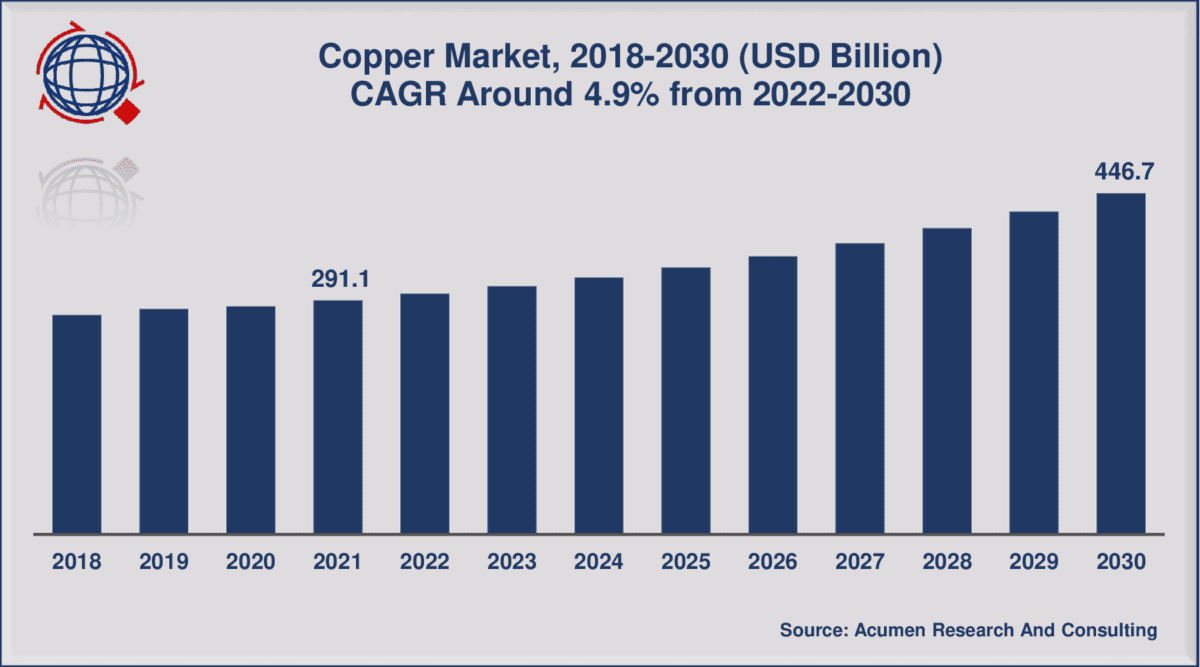

And so now could possibly be an excellent dip-buying alternative. Because the chart beneath exhibits, demand for Rio’s copper alone could possibly be set to rise strongly by to 2030 no less than.

Within the meantime, I believe the robustness of Rio’s stability sheet ought to assist it proceed paying giant dividends even when earnings underwhelm. Its net-debt-to-EBITDA ratio was simply 0.4 occasions as of June.

Grocery store Revenue REIT

Rio’s dividend yield for subsequent yr sails above the FTSE 100’s 3.5% ahead common. Grocery store Revenue REIT’s much more spectacular for the monetary yr ending subsequent June, at north of 8%.

Property shares like these might be nice methods to supply a second earnings. Below REIT guidelines, these companies should pay a minimal of 90% of annual rental income out within the type of dividends. That is in alternate for sure tax benefits.

Actual property shares like this aren’t at all times distinctive buys for passive earnings although. As rates of interest rise, earnings come below stress as web asset values drop and borrowing prices improve. This could in flip put dividends below stress.

Please observe that tax remedy relies on the person circumstances of every shopper and could also be topic to vary in future. The content material on this article is supplied for data functions solely. It isn’t meant to be, neither does it represent, any type of tax recommendation.

Nonetheless, with a raft of price cuts tipped for the following 12 months, now could possibly be an excellent time to think about Grocery store Revenue REIT. I particularly prefer it due to its concentrate on an ultra-stable a part of the property market which, in flip, supplies it with stability in any respect factors of the financial cycle.

It additionally has its heavyweight tenants (inlcing Tesco and Sainsbury’s) locked on long-running contracts, offering earnings with further visibility. The agency’s weighted common unexpired lease time period (WAULT) is round 12 years.

{kind=link}