Picture supply: Getty Pictures

Searching for the perfect progress shares to purchase within the New 12 months? Listed below are two of my favourites.

I’ve put my cash the place my mouth is and acquired them for my very own portfolio.

Video games Workshop

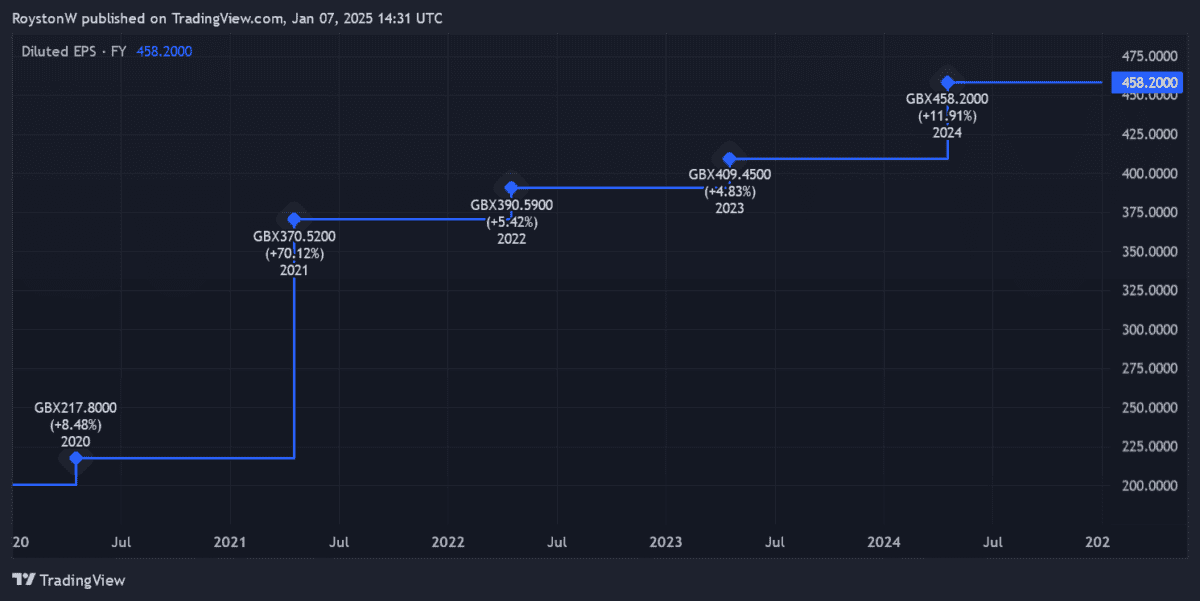

Final yr was a landmark one for tabletop gaming large Video games Workshop (LSE:GAW) because it entered the FTSE 100 for the primary time.

Earnings right here have grown persistently and at speedy tempo in recent times, because the chart beneath reveals. Tabletop wargaming isn’t everybody’s cup of tea. Nevertheless it’s rising quickly as world curiosity within the fantasy soars, and board gaming typically enjoys a renaissance.

Via its Warhammer line of merchandise, Video games Workshop is on the forefront of this booming business. And it’s aiming to enter the mainstream by launching movie and TV content material with Amazon within the subsequent few years.

It’s a transfer that might supercharge gross sales of its conventional video games techniques and create big royalty revenues in its personal proper.

Income look set to proceed rising strongly within the meantime, as new merchandise fly off the cabinets and the corporate grows its worldwide retailer property. Late November’s buying and selling replace underlined its continued trajectory, predicting pre-tax earnings of no less than £120m within the six months to 1 December, up 25% yr on yr.

This helps Metropolis predictions that annual earnings will develop 7% this monetary yr (to Could 2025). Earnings are tipped to extend one other 5% in subsequent yr as properly.

Video games Workshop’s robust outlook is mirrored by its elevated price-to-earnings (P/E) ratio of 27.2 occasions. Whereas I feel the corporate is worthy of this premium valuation, it means its shares might doubtlessly stoop if any hiccups happen.

Greggs

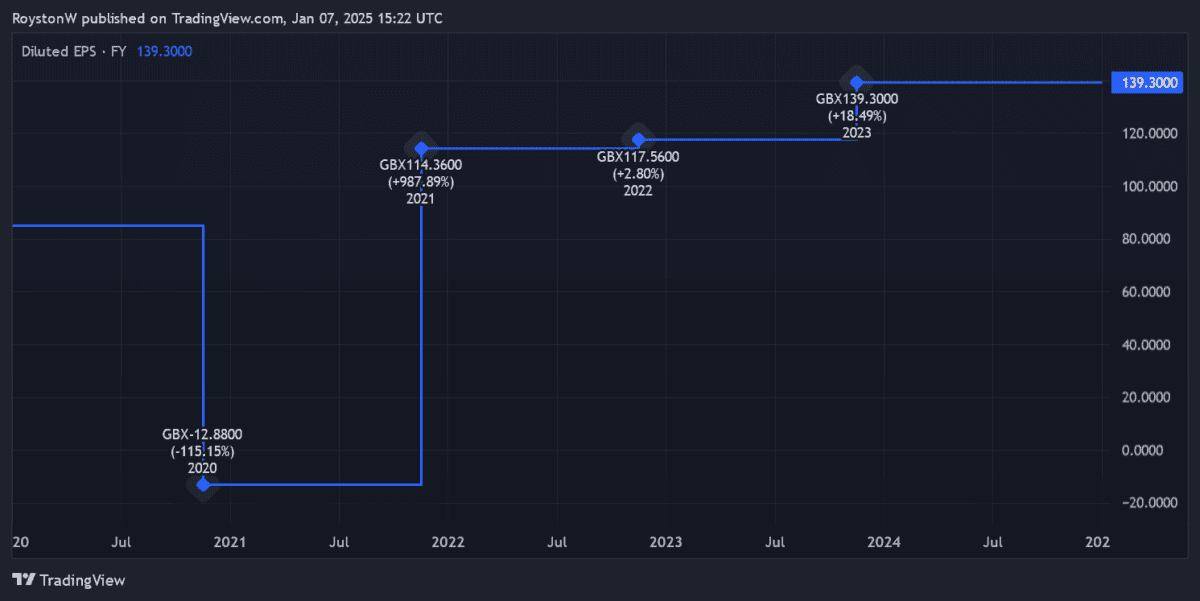

Pandemic apart, Greggs (LSE:GRG) has additionally loved spectacular earnings progress in recent times. That is thanks largely to an enlargement technique that’s pushed gross sales round three-quarters increased since 2019.

For 2024, Metropolis analysts assume the FTSE 250 firm’s earnings rose 8% yr on yr. They’re forecasting additional meaty progress — of seven% and eight% — in 2025 and 2026.

That is maybe unsurprising given Greggs’ dedication to continue to grow its retailer property from present ranges of round 2,560. It deliberate for between 140 and 160 new shops in 2024 alone, and plans to have 3,500 company-managed and franchise shops up and operating within the subsequent few years.

Competitors within the food-on-the-go market is intense and stays a menace. However Greggs’ recipe of providing generational favourites (like sausage rolls and doughnuts) at enticing costs helps it efficiently navigate this hazard. Newest financials confirmed gross sales up 12.7% between 1 January and 28 September.

The baker’s additionally successfully tailoring its providers to fulfill the wants of the fashionable client. Latest measures embody introducing a click on and acquire service, constructing drive-thru shops, and increasing opening hours into the night.

Right this moment Greggs trades on a ahead P/E ratio of 20.8 occasions. Whereas the inventory isn’t low cost, I don’t this may have an effect on its probabilities of printing additional spectacular good points following final yr’s wholesome rise.

{kind=link}