Picture supply: Getty Pictures

UK shares have largely rallied from the underside round two years in the past. Nevertheless, some have been left behind. A type of shares is Jet2 (LSE:JET2).

Whereas Jet2 is up 137% over 5 years, this comparability begins from a really low base. As an alternative, we are able to truly see that the airline’s inventory is flat versus the place it was in December 2020 — for context, the UK was in lockdown on the time.

In different phrases, zero share value progress in four-and-a-half years. And that in itself is a hazard. I like shares with momentum as a result of they’re extra more likely to attain honest worth faster.

Nonetheless, this lack of momentum is a threat I’m keen to take with Jet2. I’ve just lately added it to my portfolio. I merely imagine the inventory is vastly undervalued.

Right here’s what the charts say

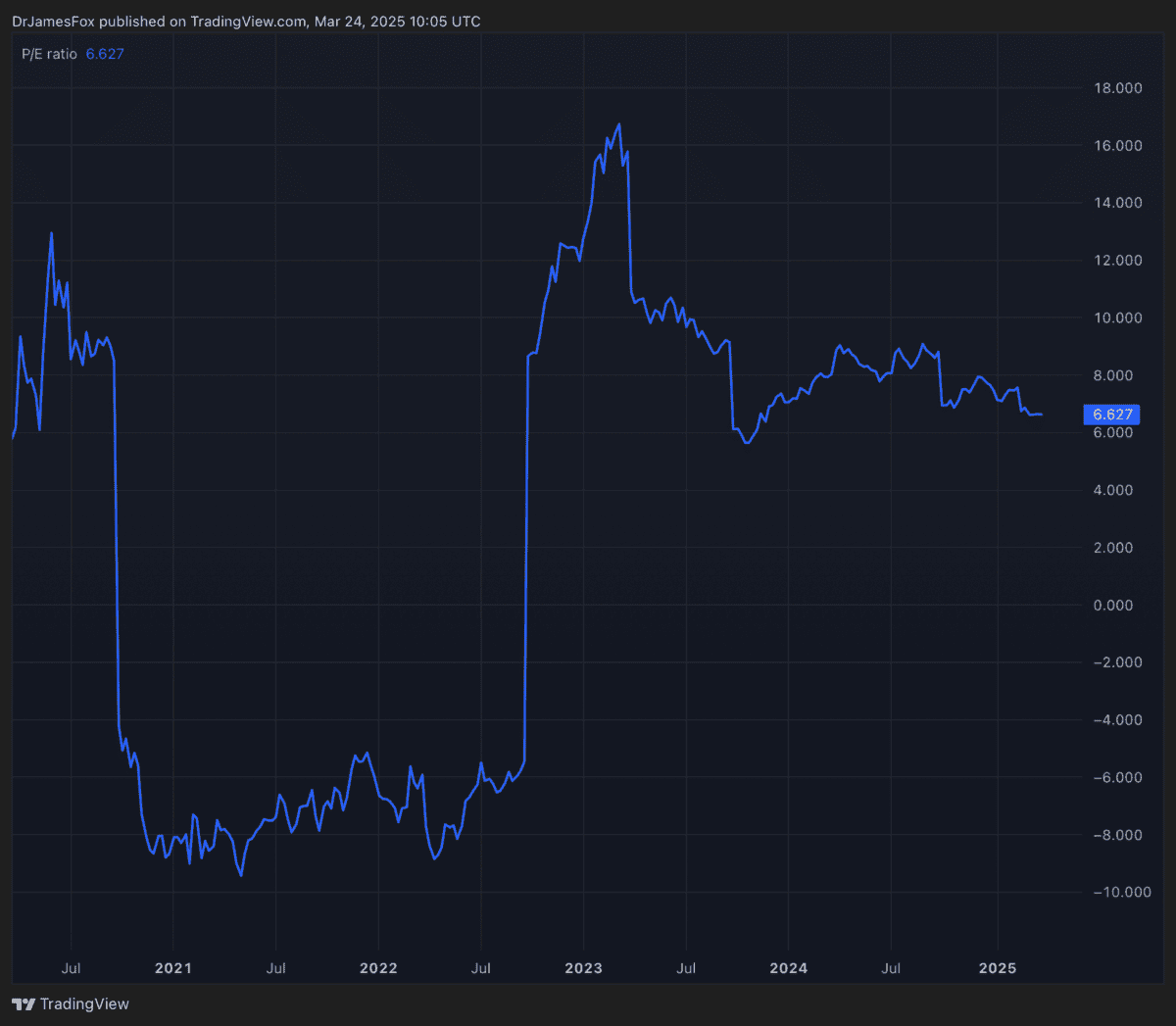

Jet2 inventory trades round seven instances ahead earnings. That’s not costly for UK-listed firms and it’s not significantly costly for airways. The worldwide airways common is presently round 7.4 instances.

The above knowledge exhibits the price-to-earnings (P/E) ratio fluctuating, nevertheless it’s again consistent with the place it was 5 years in the past. We are able to additionally observe the impression of the P/E on earnings in 2020 and 2021, when it turned damaging.

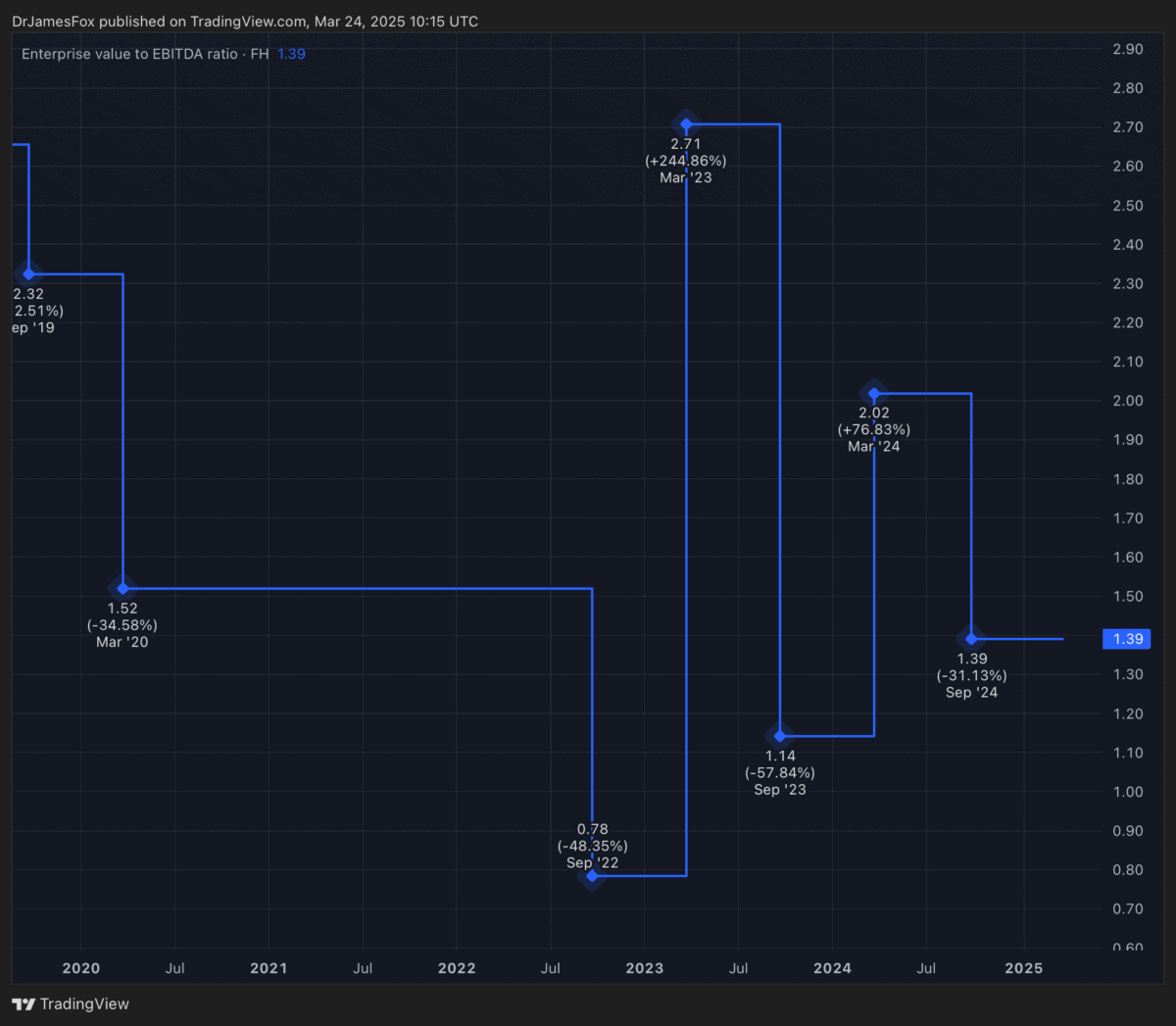

Nevertheless, the true indicator of worth is the EV-to-EBITDA ratio. Most airways don’t have a web money place, however Jet2 has £2.3bn in web money. In consequence, its EV-to-EBITDA ratio is definitely slightly shut to 1. In different phrases, it’s enterprise worth is sort of coated by only one 12 months of EBITDA (earnings earlier than curiosity, tax, depreciation, and amortisation).

By comparability, IAG trades at 5.4 instances ahead earnings and with an EV-to-EBITDA ratio of three.4. The inference right here is that Jet2 has been vastly ignored.

An organization overview

Jet2, the UK’s largest inclusive tour operator and a number one leisure airline, is strategically positioned for progress regardless of dealing with trade challenges. Analysts anticipate earnings progress over the medium time period, supported by Jet2’s increasing market presence and investments in fleet modernisation.

The Leeds-based firm has a barely older fleet, at 13.9 years, than a few of its friends. And Jet2 plans to take a position £5.7bn between 2025 and 2031 to improve its fleet, transitioning to a majority Airbus configuration and rising capability from 135 to 163 plane. The brand new A321neo plane are anticipated to boost operational effectivity with decrease gas consumption and better seating capability.

This funding aligns with trade norms, representing roughly 11.4% of projected income for 2025 and declining additional as income grows to an estimated £8.6bn by 2027. In truth, the corporate’s web money place is forecast to hit £2.7bn by 2027.

Nevertheless, traders ought to word potential dangers. Rising prices, together with wages, airport expenses, and upkeep bills, may strain revenue margins. Moreover, aggressive pricing within the European leisure market and a development in the direction of later bookings could create challenges.

Regardless of these challenges, Jet2’s robust market place, money place, valuation, and strategic investments are compelling. For this reason I’ll proceed trying so as to add to my place at present costs.

{kind=link}