Picture supply: Getty Photos

There aren’t that many FTSE 100 corporations that may declare to have posted £1bn in annual revenue. However that’s precisely what this well-liked excessive road trend retailer did when it posted its full-year outcomes this morning.

Subsequent

Subsequent (LSE: NXT) is a well-loved and recognisable excessive road trend model, specialising in clothes, footwear and residential merchandise. Established in 1982, the corporate has grown to change into a staple on the UK excessive road, working over 500 shops nationwide.

Past its bodily presence, it’s developed a profitable on-line platform catering to prospects each domestically and internationally. The retailer provides a variety of merchandise, together with males’s, girls’s, and youngsters’s trend, in addition to dwelling furnishings and equipment.

For the fiscal yr ending January 2025, Subsequent simply managed to cross the £1bn revenue milestone, posting pre-tax revenue of £1.011bn. This equates to a ten.1% enhance in annual earnings.

In the meantime, group gross sales rose by 8.2% to £6.32 bn, pushed by expectations-beating gross sales within the preliminary eight weeks of the fiscal yr. Because of this, the corporate has revised its gross sales progress forecast for the primary half of the yr from 3.5% to six.5%, resulting in an anticipated annual progress charge of 5%.

Moreover, the retailer elevated its pre-tax revenue steering by 5.4% to £1.066bn.

Tariff chaos continues

In different information this morning, President Donald Trump plans to impose a 25% tariff on all imported cars to the US. The announcement despatched ripples via world monetary markets, with the FTSE 100 taking a minor hit. The UK helps a number of main automotive producers and associated industries, all of which might undergo as markets tackle the influence of declining automobile exports to the US.

In fact automobile tariffs aren’t a problem for the agency, however whereas upcoming modifications to de-minimis customs thresholds are, they’re anticipated to have little influence on the corporate’s general gross sales and earnings. Within the EU, many of the firm’s enterprise already runs via an area subsidiary, that means it gained’t be affected by the rule change. The rest, bought through a UK entity and imported by shoppers, will face extra duties from 2028. Nonetheless, the monetary influence is anticipated to be minimal, with an estimated internet value of below £1m.

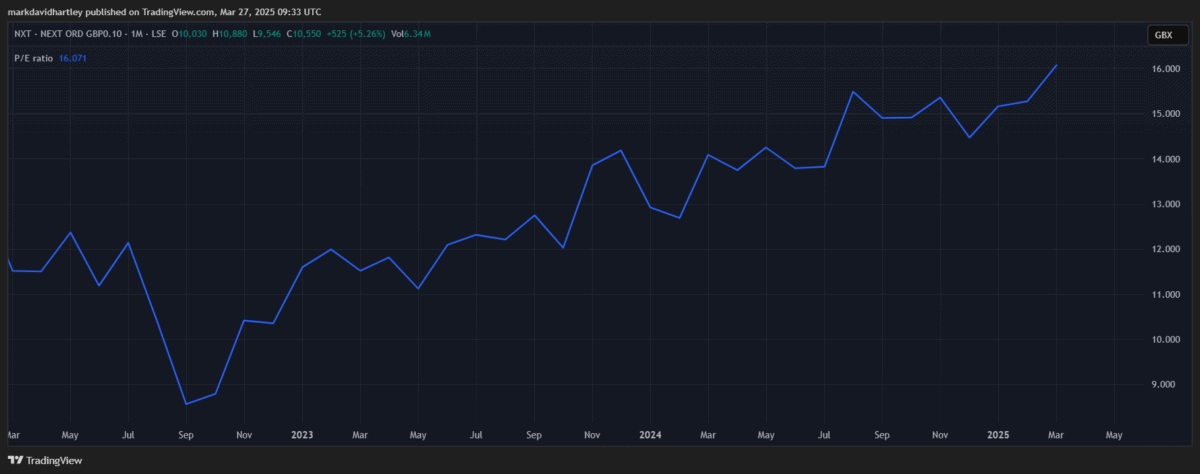

Nonetheless, the chance of losses from a broader financial downturn stays a chance. It’s additionally transferring in the direction of overvalued territory, with a price-to-earnings (P/E) ratio rising from 8.5 to 16. Add to this shifting shopper behaviour and growing competitors from the likes of Marks & Spencer, ASOS and Debenhams Group.

Whereas these particular commerce insurance policies could in a roundabout way influence the retailer, rising geopolitical tensions and market fluctuations stay a trigger for concern. All these elements might affect the corporate’s general operations and enterprise situations.

Heading in the right direction

right this moment’s numbers and monetary efficiency, there are notable indicators of sturdy administration and a resilient enterprise mannequin. The corporate’s profitable integration of on-line and bodily retail channels positions it effectively within the evolving retail panorama.

It’s doing effectively to reaffirm its place as a frontrunner inside the British trend retail sector. At this time’s outcomes reveal its skill to spice up gross sales via market adaptability. Regardless of the financial challenges, I believe this strategic strategy, mixed with a powerful market presence, might equate to a promising future for the agency.

Total, I believe it’s inventory to think about as a part of a portfolio geared toward leveraging UK progress and sidestepping the influence of US commerce tariffs.

{kind=link}