Picture supply: Getty Photos

FTSE 100 shares have (largely) come out swinging in 2025. Up 17%, the UK’s premier share index has benefitted from resilient earnings, falling inflation, and rising demand for affordable shares.

With all of those catalysts nonetheless in play, 2026 could possibly be one other yr of titanic share value beneficial properties. Naturally some blue-chip shares are more likely to carry out significantly better than others.

Barratt Redrow (LSE:BTRW) and Antofagasta (LSE:ANTO) are two FTSE shares I feel might take off subsequent yr. Wanna know why?

House run?

Buyers nonetheless doubt the housing market’s underlying energy, however I feel they’ll come round. And after they do, I feel housebuilder shares might detonate.

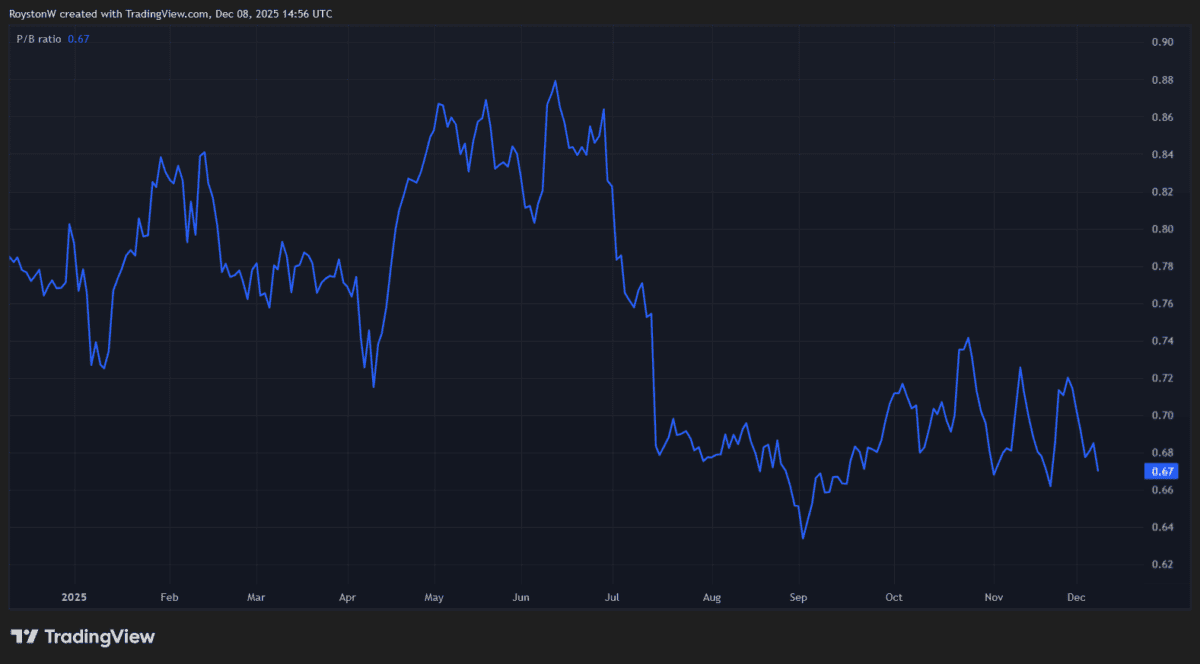

Barratt Redrow is one I feel might rebound owing to its rock-bottom valuation. The UK’s largest housebuilder has tumbled 15% in worth since 1 January, leaving it buying and selling on a price-to-book (P/B) ratio of 0.7. Any studying beneath one exhibits a inventory buying and selling beneath the worth of its property.

Housebuilders are among the many most economically delicate shares on the market. So on one hand, it’s comprehensible that Barratt’s dropped sharply since mid-summer — financial forecasts for the UK haven’t precisely been brimming with confidence.

But Barratt’s valuation nonetheless appears to be like far too low to me. And as I stated on the prime, the houses market stays fairly sturdy regardless of weak financial circumstances.

Can the market sustain the momentum although? I feel it may possibly, as lending circumstances steadily enhance. Common charges on two- and five-year mortgages at the moment are at their lowest fee since Liz Truss’ disastrous mini-Finances in 2022, based on Moneyfacts.

This displays an more and more bloody fee conflict amongst Britain’s lenders. With the Financial institution of England tipped to maintain decreasing charges subsequent yr, too, I feel issues will maintain getting higher for homebuyers.

Barratt’s rock-bottom valuation might entice critical dip-buying curiosity on this situation, driving its share value larger.

Getting began?

Antofagasta’s share value has headed in a really completely different path in 2025. It’s up a mammoth 84% since 1 January. I feel it might simply be getting began.

I’m not anticipating it to draw consideration from cut price hunters like Barratt’s shares. It trades on an excessive price-to-earnings (P/E) ratio of 31.5 instances. However the copper miner might nonetheless stride larger as costs of the economic metallic balloon.

Copper is up 32% within the yr to this point as shrinking provides have sparked panic shopping for. With the US stockpiling metallic, mine disruptions ongoing, and demand from information centres and the renewable power sectors booming, 2026 could possibly be one other sturdy yr for the purple metallic.

Citi analysts assume costs might hit $14,000 a tonne subsequent yr. They have been final round $11,600.

I like the concept of shopping for copper shares to capitalise on this chance. As Antofagasta’s share value motion exhibits, they will rise extra sharply in worth throughout bull markets than the metallic itself. This displays the ‘leverage’ impact, the place revenues balloon whereas prices stay unchanged. It’s a mix that may supercharge income.

There are dangers although. Contemporary commerce tensions and different financial shocks might harm copper demand and due to this fact costs. Antofagasta can also be prone to profits-sapping manufacturing stops, a continuing threat for mining firms.

But on steadiness, I feel it’s a prime FTSE 100 inventory — like Barratt — to focus on giant returns subsequent yr.

{kind=link}