Picture supply: Getty Photographs

One of the best time to purchase shares is when different traders are wanting elsewhere. And it’s honest to say that uncertainty round US commerce coverage has triggered a shift within the inventory market.

Because the begin of the 12 months, the FTSE 100 is up 6% whereas the S&P 500 is roughly the place it was initially of January. So does that imply it’s time for traders to take a look at shopping for US shares?

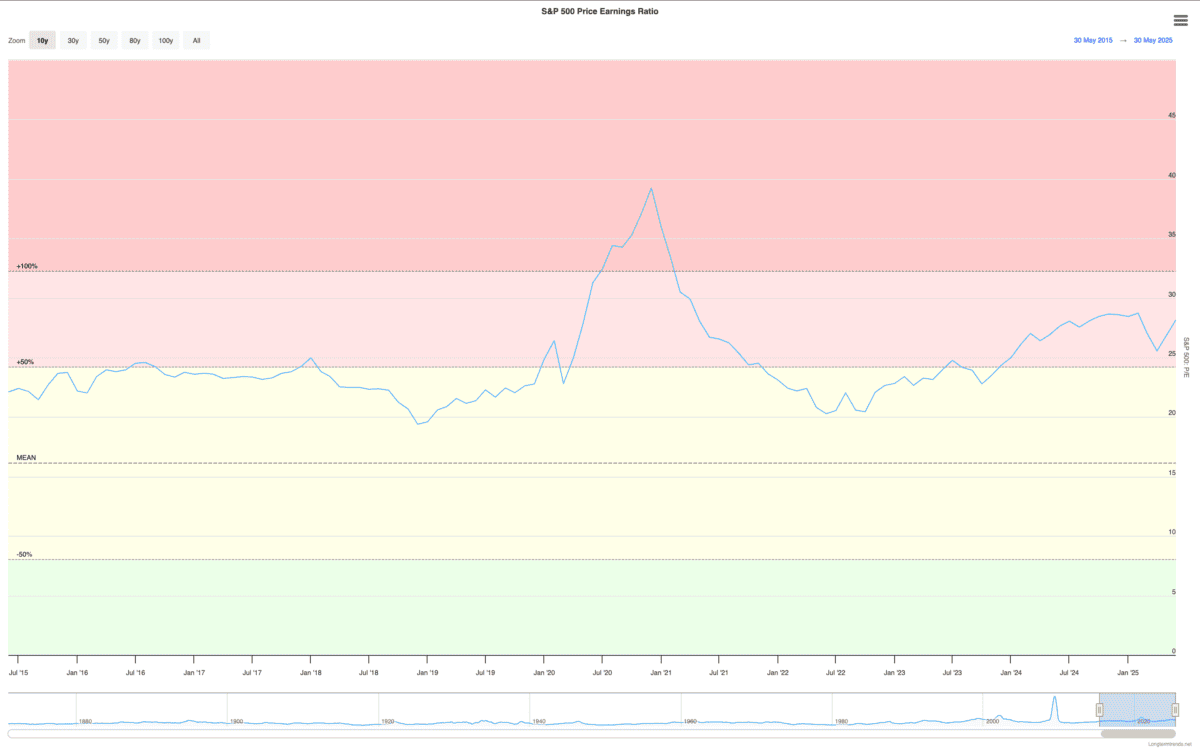

The S&P 500 doesn’t look low cost

The MSCI US Index has underperformed the MSCI World Index for the reason that begin of the 12 months. However the S&P 500 as a complete posted earnings development of round 18% within the fourth quarter of 2024.

That’s very spectacular and better earnings do make valuations extra engaging. Nevertheless, within the grand scheme of issues, the distinction is pretty marginal.

The present price-to-earnings (P/E) ratio of the S&P 500 is in the direction of the upper finish of the place it has been over the past 10 years. And historical past tells us that returns from these ranges are sometimes underwhelming.

In fact, the longer term doesn’t at all times resemble the previous. However I feel there are alternatives in particular person shares that look rather more engaging.

Not all shares are identical

The S&P 500 is in constructive territory for the reason that begin of the 12 months, however not each inventory has carried out the identical. To this point, one of many worst-performing sectors in 2025 has been power.

Total, power shares are down round 3.5% and a few particular person shares have fared a lot worse. However that is the type of shift that I feel can generate alternatives for traders.

A sector falling out of favour with the inventory market may give traders an opportunity to purchase the very best shares at unusually good costs. Proper now, I feel ConocoPhillips (NYSE:COP) is perhaps a great instance.

The inventory is down nearly 14% for the reason that begin of the 12 months, however the firm’s long-term benefits stay intact. And it has bold plans for shareholder returns.

A possible power alternative

In 2024, ConocoPhillips generated simply over $8.25bn in free money and it has bold plans to develop this by $6bn between now and 2029. If it may do that, the present share worth seems to be very low cost.

The agency’s acknowledged goal includes the corporate producing nearly 15% of its present market worth in free money annually from 2029. However loads will depend on what occurs to grease costs within the subsequent few years.

That is the largest danger with ConocoPhillips shares. Its future ambitions are primarily based on a median oil worth of $70 per barrel and it’s price noting the value of WTI crude is presently 10% beneath this.

Traders due to this fact shouldn’t depend their chickens prematurely. However with a major quantity of untapped stock obtainable at lower than $40 per barrel, there might nonetheless be good returns on the best way.

Grasping when others are fearful

US shares as a complete don’t seem like an apparent shopping for alternative to me for the time being. But it surely’s a distinct story with the out-of-fashion power sector and ConocoPhillips is an effective instance.

The agency is presently set to return nearly 100% of its market worth to shareholders over the following 10 years. And with bold development plans forward, I feel it’s price contemplating at right now’s costs.

{kind=link}