Picture supply: Getty Pictures

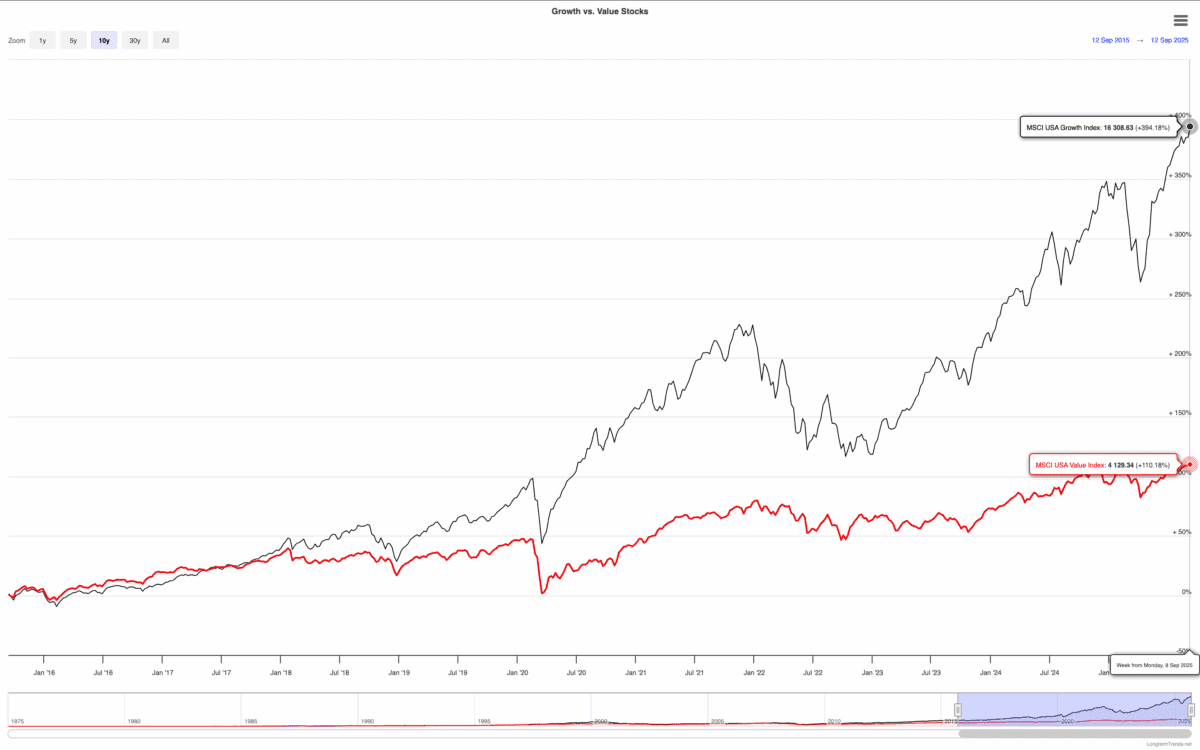

Over the past 10 years, progress shares have outperformed worth shares by some margin – particularly within the US. The MSCI USA Development index is up 394%, whereas the MSCI USA Worth Index has climbed 110%.

Proper now, the hole between progress and worth shares is traditionally vast. However is that this an indication of issues to come back, or an indication that worth shares are about to bounce again in a giant means?

Warren Buffett

In response to Warren Buffett, the distinction between progress and worth investments doesn’t make a lot sense. However this can be a uncommon event (I can solely consider one different) the place I don’t agree.

Buffett’s level is that each one investing is about making an attempt to purchase shares for lower than they’re value. And determining the worth of a inventory entails taking a view concerning the firm’s future progress.

I agree with all of this, however I don’t assume it means there’s no distinction between progress and worth. In my very own portfolio, I’ve shares that I personal for various causes.

I personal some shares as a result of I count on future money flows to be increased – these are progress shares. In others, it’s as a result of the share value doesn’t mirror present earnings – these are worth shares.

Time for a correction?

In the meanwhile, the hole between progress shares and worth shares would possibly nicely be the most important it has ever been. And when this has been the case prior to now, issues have usually corrected sharply.

I don’t assume, although, that this implies worth shares are set to catch up. Traditionally, the distinction narrowing has been the outcomes of issues which have precipitated crashes within the inventory market usually.

The distinction in valuation is likely to be unjustified (or it may not). However there’s no rule that claims that simply because it’s expanded it has to contract within the close to future.

I do assume, although, that the unusually vast discrepancy in valuations means it’s an fascinating time to be taking a look at worth shares. And some look fascinating at at present’s costs.

A inventory to contemplate

Polaris (NYSE:PII) is one instance. Shares within the leisure automobile firm are down round 30% over the past yr because the agency has needed to cope with a varied challenges – most notably, tariffs.

This has had an impact on each revenues (which have fallen) and internet earnings (which has turned unfavorable). And the possibility of inflation within the US resulting in increased rates of interest is an ongoing threat.

I feel, nevertheless, that issues aren’t as unhealthy as they appear. The web earnings loss was attributable to non-cash impairment fees, which might’t be ignored completely however must be one-off in nature.

The corporate’s robust manufacturers and in depth vendor community ought to put it in a robust place when demand recovers. And with an unusually excessive 4.5% dividend yield, I feel it’s value contemplating.

Development and worth

As progress shares have outperformed worth shares, the hole between the 2 has reached its widest degree in historical past. And the relative low cost is an indication the latter are out of vogue.

This doesn’t have to alter within the close to future, however long-term traders ought to take word. Whereas not all worth shares are the identical, I feel Polaris is a top quality identify that’s value testing.

{kind=link}