Picture supply: Getty Photos

Information concerning the State Pension isn’t out of the headlines. Neither is theory over future dwelling requirements for retirees, emphasising the significance of long-term monetary planning with pensions or financial savings merchandise just like the Particular person Financial savings Account (ISA).

Britain isn’t alone in going through a retirement disaster. Deteriorating public funds, mixed with ageing populations, elevate questions on how governments internationally will have the ability to fund future pensions.

It’s a sobering thought. Nevertheless it’s by no means too late to begin constructing wealth to keep away from monetary hardship in later life. Let me present you ways a diversified fund may assist safeguard one’s monetary future.

Heed the warnings

Feedback on Monday (21 July) from the UK authorities underline the ticking timebomb going through Britons at present.

In line with Division for Work and Pensions (DWP) analysis, folks retiring in 2050 can be 8% — or £800 — worse off than these exiting the workforce at present.

To handle this disaster, the federal government mentioned it’s resurrecting the Pensions Fee, which is able to “look at the complicated limitations stopping folks from saving sufficient for retirement“. However that’s not all — its function can even be to “look at the pension system as an entire and take a look at what’s required to construct a future-proof pensions system that’s robust, honest and sustainable“.

On prime of this, one other authorities evaluation will analyse the age at which individuals can start claiming the State Pension.

The present pension age of 66 is scheduled to rise to 67 between 2026 and 2028, and once more to 68 between 2044 and 2046. However some economists and business consultants are warning these adjustments may very well be introduced ahead.

Concentrating on a £44k passive revenue

I don’t find out about you. However I don’t need to put myself on the mercy of fixing authorities coverage. I need to retire at an honest age, and to get pleasure from a cushty lifestyle once I do.

My plan is to construct my very own retirement fund with money, shares, trusts, and funds, utilizing a spread of ISAs and my Self-Invested Private Pension (SIPP). By prioritising investing within the inventory market, I believe I can obtain a long-term common annual return of 8% whereas nonetheless successfully managing threat.

At that price of return, a month-to-month funding of simply £500 over 30 years would create a retirement nest egg of £745,180. At this stage, one may get pleasure from an annual passive revenue of £44,711 in retirement if invested in 6%-yielding dividend shares.

And that’s excluding any doable assist from the State Pension.

Wealth constructing fund

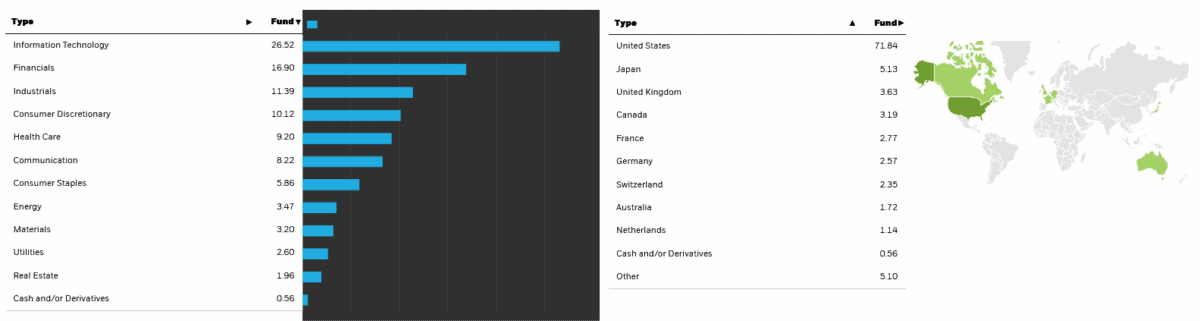

World funds just like the iShares Core MSCI World Index (LSE:IWDG) may be highly effective weapons in serving to me obtain this. Diversification throughout areas and sectors ship wonderful threat administration whereas not compromising the chance to make life-changing returns.

Certainly, this exchange-traded fund (ETF) has delivered a mean annual return of 10.9% since its creation in 2017.

Fairness-based autos like this will ship disappointing returns throughout market downturns. However as this iShares fund has proven, over the long run they will successfully harness the potential of the inventory market and ship nice returns. Main holdings right here embrace Nvidia, Amazon, and Berkshire Hathaway. In whole it holds shares in 1,324 international shares.

With publicity to highly effective progress sectors like IT and monetary providers, I believe this fund may stay a superb wealth builder. It’s certainly one of a number of funds I believe demand severe consideration.

{kind=link}