Picture supply: Getty Photos

FTSE 250 retailer WH Smith (LSE:SMWH) doesn’t instantly soar out as a inventory to think about shopping for. It trades at a price-to-earnings (P/E) a number of of 29 and there are higher moats round sandcastles.

On nearer inspection although, there’s much more than meets the attention. The enterprise is healthier than preliminary appearances recommend and the share worth is definitely cheaper than it appears.

Bodily retail?

WH Smith has an unimpressive bodily retail operation. In a world of on-line purchasing and fierce excessive avenue competitors, this a part of the enterprise doesn’t have a lot to distinguish itself.

The newest outcomes bear this out – gross sales within the firm’s excessive avenue shops are down 4% from a yr in the past. However there’s much more to the enterprise than struggling brick-and-mortar shops.

Round 75% of the FTSE 250 firm’s income comes from its Journey division – shops positioned in practice stations, airports, and so forth. And issues look very totally different on this a part of the organisation.

Journey gross sales are rising at round 10% a yr and the agency sees alternatives to maintain increasing. The outcome’s a discount within the quantity of the corporate’s revenues that come from excessive avenue gross sales.

It needs to be famous that this makes it extra closely uncovered to fluctuations in journey demand – which could be cyclical. And whereas this may occasionally develop over time, it’s a threat buyers ought to pay attention to.

Importantly although, airports and practice stations are good retail areas – there’s much less competitors and the specter of e-commerce is virtually zero. And that tremendously improves WH Smith’s prospects.

Is it low-cost?

The above however, it’s pure to suppose 29 occasions earnings is so much to pay for a inventory like this. And I agree – however the firm’s P/E a number of’s a bit deceptive for the time being.

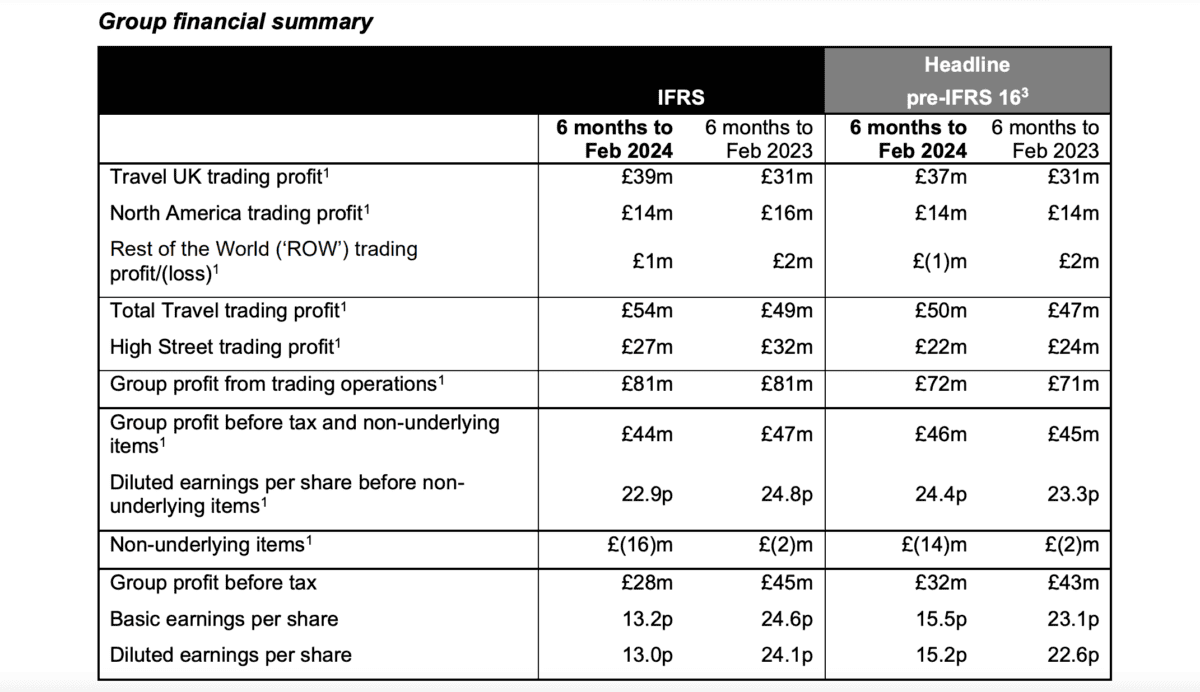

Within the six months main as much as February 2024, the corporate generated 13p in earnings per share (EPS), down from 24.1p the earlier yr. That’s regardless of an 8% improve in revenues.

Supply: WH Smith interim outcomes 2024

The reason being the agency incurred £16m in bills for ‘non-underlying objects’ — up from £2m in 2023. These are related to writing down the worth of excessive avenue shops and ending sure contracts.

Traders ought to notice two issues about these. The primary is that they’re – in WH Smith’s view – one-off and the second is that they’re usually bills that contain no money leaving the enterprise.

In consequence, these accounting prices arguably give a distorted image of the corporate’s ongoing incomes energy. Leaving them apart, the corporate’s EPS got here in at round 23p.

On this foundation, its EPS over the past 12 months have been nearer to 77.6p. And at in the present day’s costs that means a P/E a number of of round 18.

A possible discount

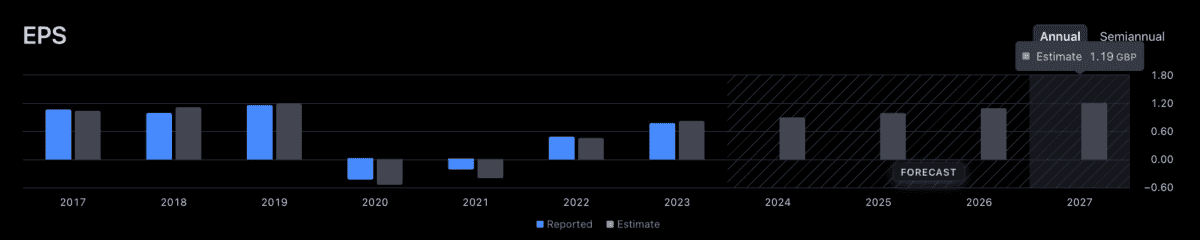

Analysts predict income to develop over the following few years. The anticipated ahead P/E a number of is 14 and the consensus is for EPS to achieve £1.19 by 2027.

WH Smith analyst EPS estimates

Time will inform if these estimations are correct. However buyers ought to notice that the FTSE 250 firm’s considerably stronger than it seems to be at first sight and the inventory’s virtually definitely cheaper. It could be price contemplating.

{kind=link}