Former Binance CEO, Changpeng Zhao (CZ), lately said that the UAE generates surplus energy so as to cowl “three days” of excessive demand every year, making Bitcoin a purchaser of final resort for power that might in any other case go unused.

Stripping away the specifics, the logic holds: mining turns curtailed or stranded electrical energy into income when no different offtaker desires it.

The query for 2026 is not whether or not surplus might be mined, however whether or not that surplus is structural sufficient to contract, and whether or not miners can maintain their place as AI and high-performance computing push up the clearing value for agency provide.

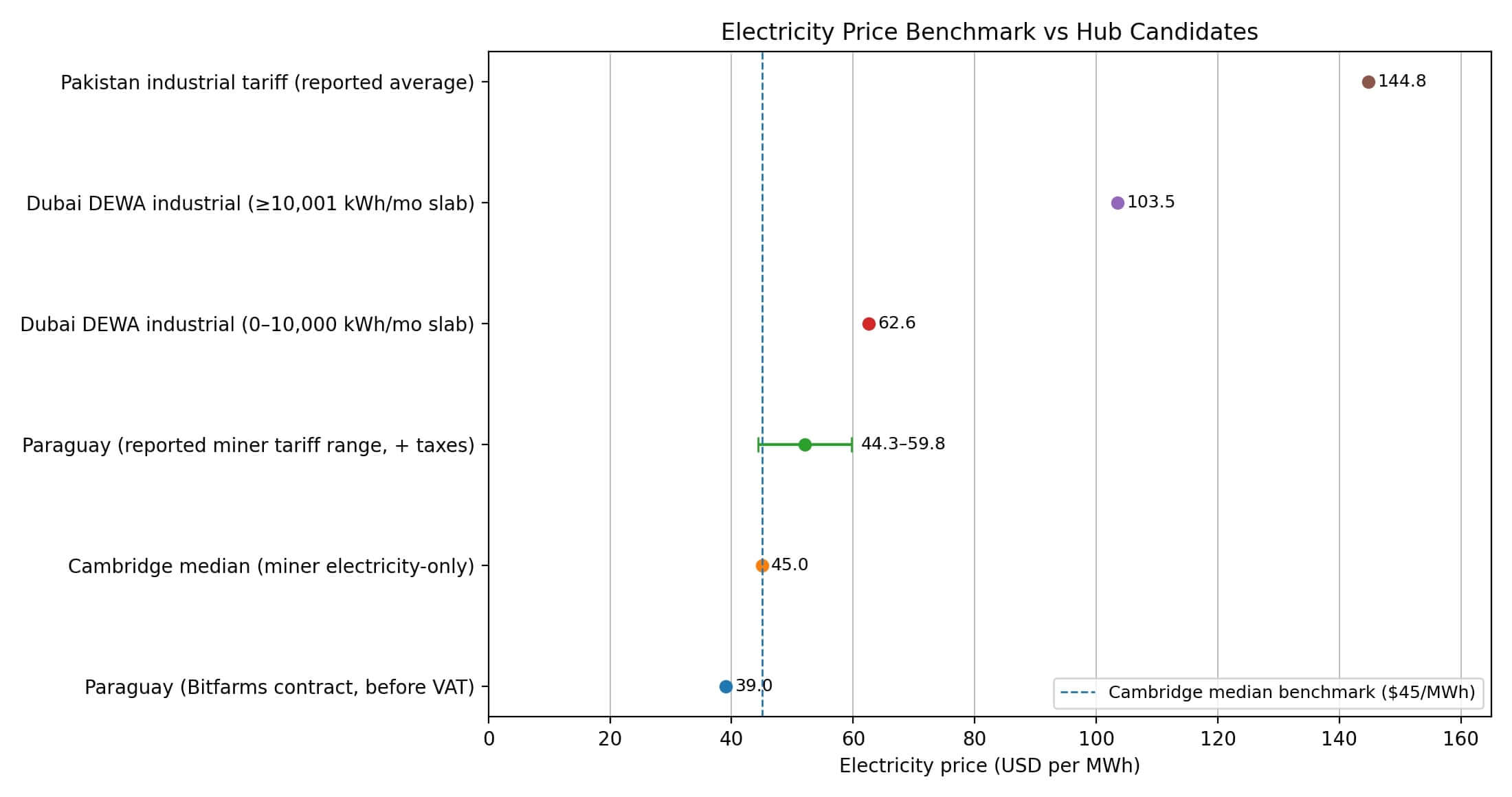

The economics are easy. Electrical energy accounts for greater than 80% of miners’ money working bills, in keeping with Cambridge’s Digital Mining Trade Report.

The identical report cites a median electricity-only price of round $45 per megawatt-hour and notes that surveyed miners curtailed 888 gigawatt-hours of load in 2023, roughly 101 megawatts of common withheld capability.

That curtailment determine helps the flexible-load thesis: miners can swap off when grids want aid or when costs spike, making them helpful to utilities managing intermittency or congestion.

Geography tells the remainder of the story. Whereas imperfect in methodology, the Cambridge Bitcoin Electrical energy Consumption Index Mining Map tracks the place hashrate concentrates, although the information carries caveats, similar to estimates lagging by one to a few months, and VPN or proxy routing can inflate shares in international locations like Germany and Eire.

Nation attribution depends on geolocating IP addresses, a technique that’s delicate to routing habits and topic to different inference limitations.

Inside these constraints, the map reveals mining distributed throughout jurisdictions with one factor in frequent: entry to energy that is both low-cost, stranded, or each.

Pakistan turns overcapacity into coverage

Pakistan made probably the most express wager. The federal government introduced plans to allocate 2,000 megawatts within the first section of a nationwide initiative break up between Bitcoin mining and AI information facilities, with CZ named strategic adviser to the Pakistan Crypto Council.

The Finance Ministry framed it as a approach to monetize surplus era in areas with extra power, turning underutilized capability right into a tradable asset.

Two thousand megawatts working constantly would generate 17.52 terawatt-hours yearly. With trendy mining fleets working at 15 to 25 joules per terahash, that energy might theoretically assist 80 to 133 exahashes per second of hashrate earlier than accounting for curtailment, energy utilization effectiveness, or downtime.

The size issues lower than the construction.

What sort of contracts will miners signal, interruptible or agency baseload? Which areas get chosen, and the way sturdy is the coverage if tariffs rise or IMF stress intensifies?

Pakistan’s initiative alerts that “additional electrons” can grow to be a nationwide export, however execution will decide whether or not 2,000 megawatts materializes as a hub or only a headline.

Surplus by design, not accident

The UAE’s alternative is not perpetual surplus, however it’s surplus-by-design.

Peak demand in Dubai reached 10.76 gigawatts in 2024, up 3.4% year-over-year, concentrated in summer season months when cooling dominates load.

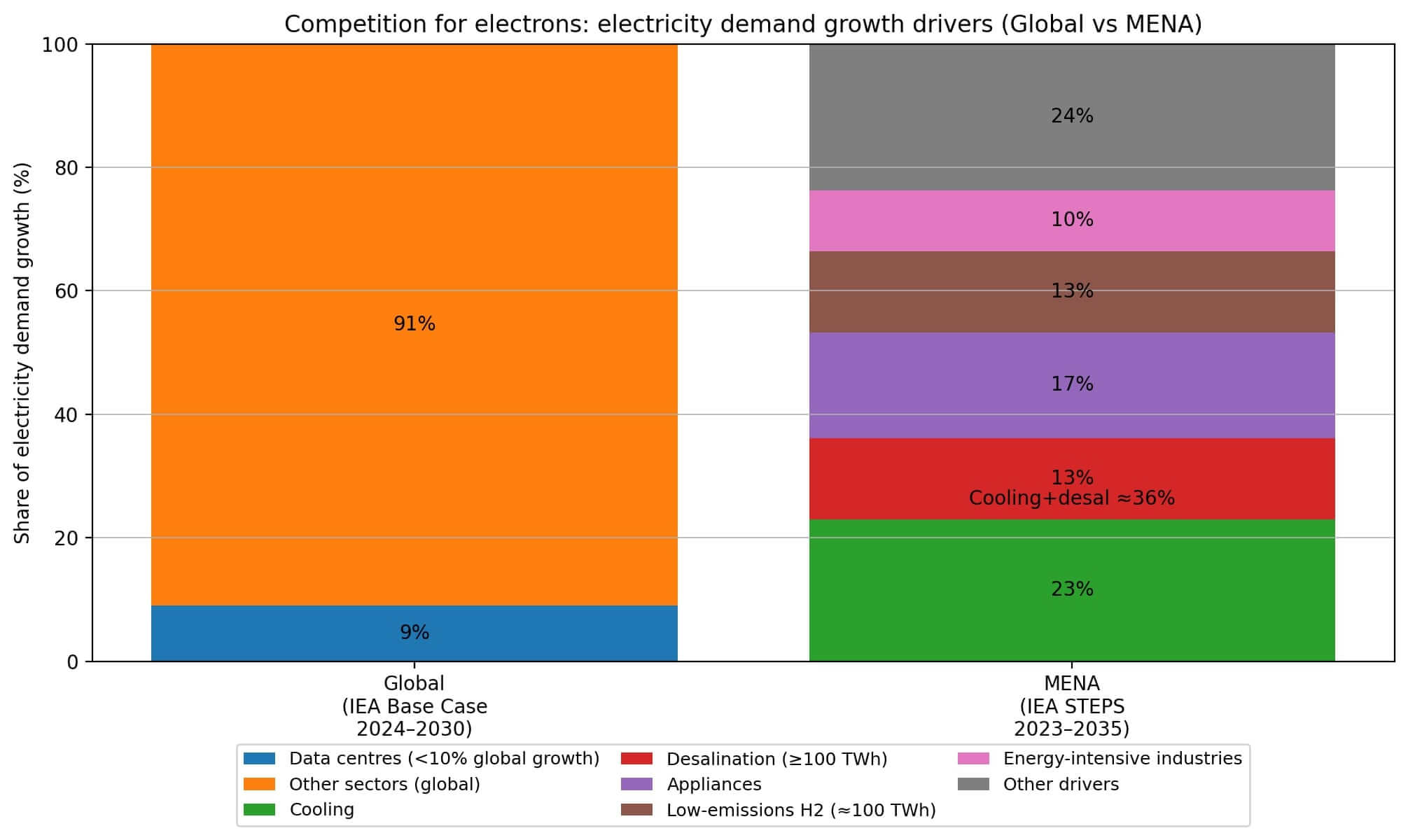

The Worldwide Vitality Company (IEA) initiatives that cooling and desalination will account for near 40% of electrical energy demand progress within the Center East and North Africa via 2035, with information facilities explicitly named as one other rising load supply.

That creates a selected opening for miners: utilities construct techniques to deal with excessive summer season peaks however want year-round monetization, normalization, and grid stability throughout off-peak intervals.

Miners win the place they will supply extra flexibility than AI or HPC consumers, similar to curtailment-ready masses that soak up energy others cannot take due to location, congestion, or dispatch constraints.

Bitcoin miners can swap off right away, whereas datacenters require steady operation, making curtailment and grid administration way more troublesome.

The area’s buildout tendencies favor baseload capability that outpaces seasonal demand, however the identical IEA outlook that flags information facilities as a driver of demand means miners face direct competitors for the electrons they want.

The hub case depends upon whether or not utilities worth dispatchable load sufficient to cost it attractively, or whether or not agency offtake contracts with AI consumers crowd out mining altogether.

When surplus turns into contested

Paraguay illustrates what occurs when surplus energy attracts miners, solely to set off a backlash.

The nation’s hydro capability attracted operators in search of low-cost electrical energy, however tariff adjustments repriced that benefit. Miners now reportedly pay between $44.34 and $59.76 per megawatt-hour plus taxes, and native trade sources cited 35 firms ceasing operations after the rise.

Legislation No. 7300 tightened penalties for electrical energy theft linked to unauthorized crypto mining, elevating most sentences to 10 years and permitting the confiscation of apparatus.

Nonetheless, actual capital nonetheless flows in. HIVE accomplished Section 1 infrastructure at a 100 megawatt facility backed by a totally energized 200 megawatt substation, signaling that some operators see sturdy economics even after repricing.

The stress is evident: hydro surplus creates the preliminary draw, however as soon as miners scale, the state re-prices energy when it realizes they seem to be a concentrated, taxable offtaker, or native grid constraints and noise externalities construct political stress.

Paraguay’s trajectory reveals how a hub can flip if social license breaks, making coverage sturdiness a first-order variable in any site-selection mannequin.

What really makes a hub

Mining hub viability in 2026 comes all the way down to a components: delivered price per megawatt-hour occasions contract flexibility occasions coverage sturdiness, measured in opposition to what AI and HPC consumers are keen to pay, grid shortage, and foreign-exchange or import friction.

Three eventualities play out throughout these variables.

Within the first, curtailment gluts persist: renewables add quicker than grids can soak up, curtailment rises, and miners win as versatile offtake. Hydro- or seasonal-surplus jurisdictions with weak transmission, similar to Paraguay, or international locations explicitly monetizing overcapacity, similar to Pakistan, are the likeliest hubs.

Within the second, AI outbids miners for agency energy. Knowledge facilities search long-term agency provide, pushing miners into interruptible, congestion-prone, or stranded pockets. Hubs emerge the place miners can entry interruptible pricing or “can’t-export” power quite than prime agency capability.

Within the third, political repricing or backlash reshapes the panorama. Governments increase tariffs as soon as miners scale or when households see shortages or noise. Paraguay turns into the template: a hub flips when the economics that attracted miners get recalibrated by the identical state that constructed them.

The IEA’s framing issues right here. World electrical energy demand is forecast to develop at a roughly 4% annual price via 2027, pushed by industrial output, air-con, electrification, and information facilities.

Renewable capability additions are accelerating, however grid integration lags. That lag creates the curtailment and congestion that miners can monetize, however it additionally means surplus is a shifting goal.

The hubs that survive 2026 aren’t simply cheap-power jurisdictions, but additionally locations the place curtailment or congestion is prone to persist, regulation tolerates mining as dispatchable load, and miners can compete with or complement AI and HPC for electrons.

The guidelines

Six variables decide whether or not a jurisdiction turns into a mining hub or only a headline.

Surplus sort is the primary. Is it hydro seasonality, stranded fuel, flare mitigation, or nuclear baseload off-peak? Every has completely different persistence and contractability.

The delivered price and contract construction comply with because the second variable. What is the all-in value per megawatt-hour, and is the contract interruptible? Who bears congestion danger, and is there compensation for curtailment?

Then comes the ASIC import and logistics, similar to customs duties, delivery lanes, spare elements availability, and capital controls, all of which have an effect on speed-to-market and operational danger.

Coverage sturdiness is the fourth variable: tariff repricing danger, licensing necessities, sudden bans, and theft enforcement decide whether or not a hub stays a hub.

Local weather, cooling, and water additionally play an element. Air-cooling limits, immersion feasibility, and warmth or noise externalities constrain the place large-scale operations can function with out triggering native opposition.

The final variable is offtake competitors: AI and HPC demand progress is now explicitly mirrored in electrical energy demand forecasts. Hubs should assume competitors for “good electrons,” not simply low-cost ones.

Pakistan’s 2,000 megawatt plan is the clearest sign that governments see surplus electrical energy as an exportable asset class, with mining as one monetization path.

Whether or not that path results in 2026’s subsequent main hubs depends upon execution, together with contract phrases, web site choice, and whether or not the political consensus holds as miners begin consuming gigawatt-hours at scale.

CZ’s thesis about Bitcoin as a purchaser of final resort is appropriate in precept. The apply is messier, contingent on grids that may’t soak up renewables quick sufficient, states that tolerate versatile masses, and miners who can keep aggressive as information facilities bid up the value of agency energy.

The hubs that emerge would be the ones the place these situations align lengthy sufficient to construct infrastructure and signal contracts that survive the primary tariff revision or the primary summer season blackout.

{kind=link}