Picture supply: Getty Photographs

Greggs‘ (LSE: GRG) shares have fallen 13% up to now month. This flaky run comes after the FTSE 250 bakery chain reported a slowdown in gross sales within the third quarter.

Regardless of this pullback, the inventory’s nonetheless returned 78% over 5 years, together with dividends. That market-beating achieve’s been pushed by a 75% enhance within the agency’s income and a greater than doubling of income.

However what in regards to the future? Listed below are the newest development forecasts for the following few years.

Metropolis estimates

If forecasts show appropriate, Greggs’ income and earnings will preserve chugging increased. This might lay the foundations for additional share value development.

| 12 months | Income | Annual Development |

|---|---|---|

| 2024 | £2.03bn | 12.2% |

| 2025 | £2.23bn | 9.9% |

| 2026 | £2.44bn | 9.4% |

| 2027 | £2.69bn | 10.2% |

We will see that Greggs is anticipated to develop its high line round 10% on common over the following few years. Most retailers would snap your hand off for those who supplied them that regular development outlook.

Metropolis analysts additionally anticipate that earnings per share (EPS) may also expertise wholesome development, resulting in changes within the forward-looking price-to-earnings (P/E) ratio.

| 12 months | EPS | P/E ratio |

|---|---|---|

| 2024 | 135p | 20.4 |

| 2025 | 149p | 18.5 |

| 2026 | 161p | 17.1 |

| 2027 | 183p | 15.0 |

The baker rolls on

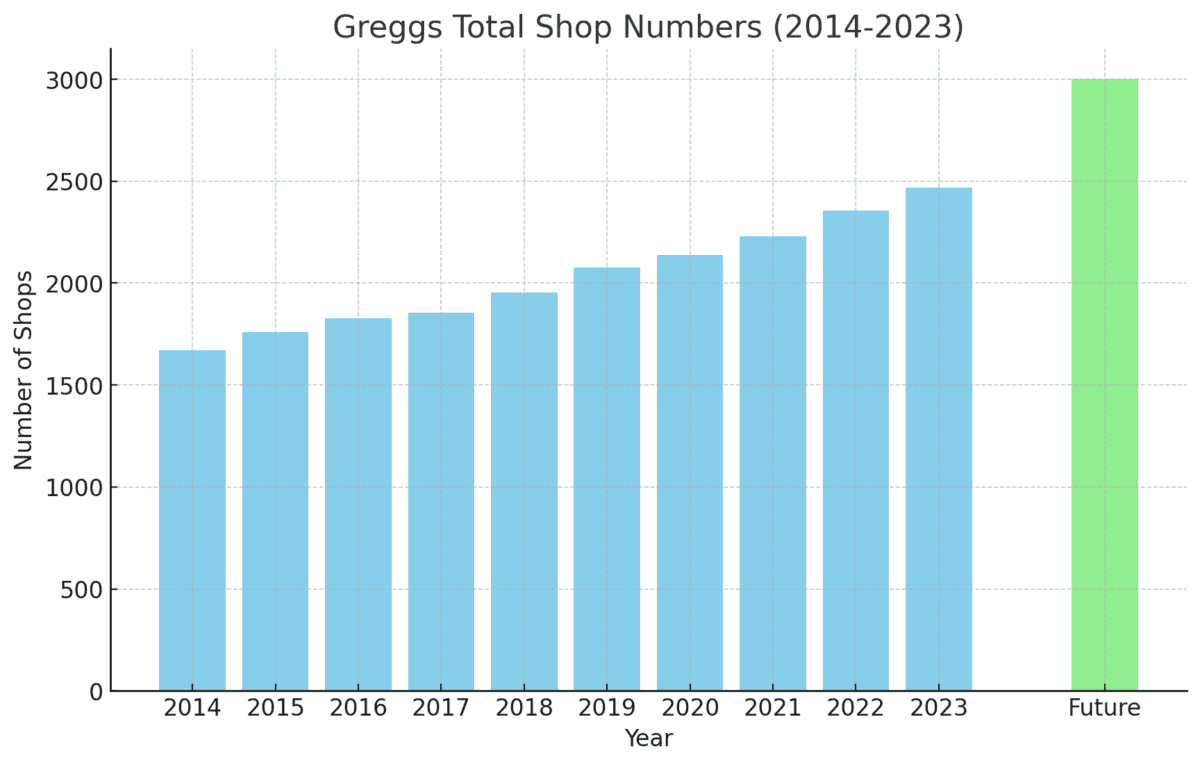

The expansion story for Greggs centres round its march in the direction of 3,000+ retail areas. It’s on monitor to open 140-160 internet new outlets in 2024, together with round 50 relocations.

As of 28 September, it had 2,559 outlets buying and selling (comprising 2,016 company-managed shops and 543 franchised items).

CEO Roisin Currie mentioned the climate in July and riots throughout England in August didn’t assist gross sales within the third quarter. But like-for-like gross sales nonetheless rose 5% in company-managed outlets, regardless of this “difficult” market. Administration maintained confidence in its full-year outlook.

Trying forward, Greggs is well-positioned to serve the night market by means of each walk-in and supply by way of Simply Eat and Uber Eats. It continues to increase its presence inside supermarkets and a few Primark shops.

The inventory’s buying and selling at round 21 occasions earnings, which is consistent with its common over the previous few years. Metropolis analysts have a 3,332p consensus share value goal, about 19% increased than the present 2,790p. In fact, there’s no assure it can ever attain this goal.

A shift in consuming habits?

As a shareholder, I do see a few dangers on the horizon. The most important is that we all of a sudden attain peak Greggs within the UK. That’s, a saturation level that results in the agency’s development slowing to a crawl (or worse). We’ve seen up to now month how shortly the share value can pull again if development disappoints.

One other danger is a possible rise in more healthy consuming. This could possibly be given a shot within the arm by weight-loss medication that cut back cravings for the treats that Greggs sells. Whereas the agency’s launched more healthy menu choices like salad bins and rice bowls, a change in consuming habits would current challenges.

My takeaway

Weighing issues up, I reckon there’s loads to love in regards to the inventory. The corporate has a singular model, underappreciated pricing energy, and a excessive return on capital (that means it’s solidly worthwhile).

There’s additionally a dividend, which has constantly risen like a Steak Bake within the oven. Nothing’s assured after all, however the agency additionally has a monitor document of generously serving up the occasional particular dividend.

If Greggs exhibits any additional value weak point, I would snap up a number of extra shares.

{kind=link}