Picture supply: Getty Photographs

Nvidia (NASDAQ: NVDA) inventory took a little bit of a bruising in January, falling 13% at one level. Nonetheless, it’s bounced again and is now 3.4% larger in 2025. Over 5 years, it’s up by a scarcely plausible 1,817%!

The AI chip king is because of launch its This fall 2025 earnings on 26 February. Right here, I’ll check out the newest forecasts heading into the outcomes report.

Unimaginable development

Since ChatGPT was launched in late 2022, Nvidia’s quarterly outcomes have blown away Wall Road’s estimates.

The desk beneath reveals the income and earnings per share (EPS) figures, together with the shock outstripping of EPS expectations.

| Quarter* | Income | Income shock | EPS | EPS shock |

|---|---|---|---|---|

| Q1 24 | $7.2bn | 10.1% | $0.11 | 18% |

| Q2 24 | $13.5bn | 20.7% | $0.27 | 29.7% |

| Q3 24 | $18.1bn | 11.2% | $0.40 | 18.5% |

| This fall 24 | $22.1bn | 8.4% | $0.52 | 12.3% |

| Q1 25 | $26bn | 5.8% | $0.61 | 9.2% |

| Q2 25 | $30bn | 4.4% | $0.68 | 5.4% |

| Q3 25 | $35.1bn | 5.8% | $0.81 | 8.3% |

As we are able to see, Nvidia was crushing estimates by double digits round a yr in the past. Nonetheless, because the AI revolution has matured and analysts have a greater grip on demand for chips, these surprises have understandably fallen into the one digits.

After all, that’s nonetheless spectacular, and it means Nvidia has crushed estimates on each the highest and backside traces each single quarter for the reason that begin of 2023. And over the interval, it has added a mind-boggling $2.8trn in market capitalisation!

For This fall 25, Wall Road expects income of $38bn and EPS of $0.84. That will symbolize distinctive respective development of 72% and 64%.

These are the headline figures that buyers ought to look out for. Although the factor that can in all probability resolve the course of the share value afterwards is ahead steerage for Q1 26. Buyers will wish to know that AI chip demand goes to stay sturdy this yr.

Proper now, analysts are forecasting income of $41.7bn and EPS of $0.91 for the present quarter (Q1). If the corporate revises this upwards, the inventory might bounce larger, and vice versa.

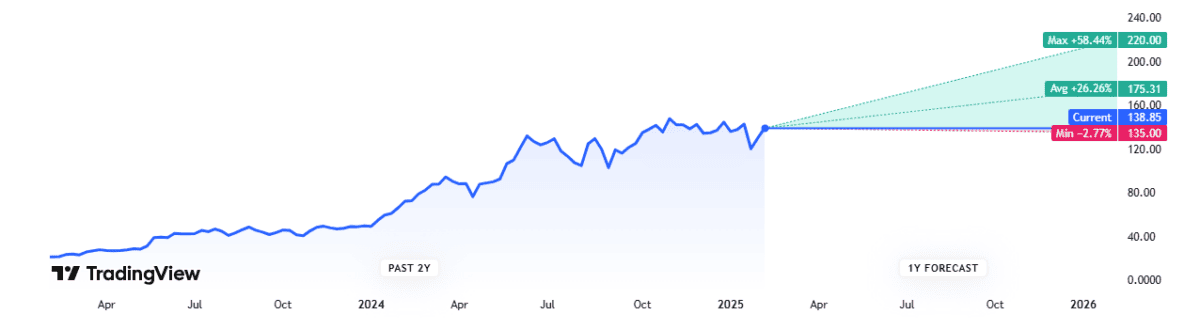

Value goal

Dealer share value targets ought to at all times be taken with a pinch of salt, particularly relating to a risky inventory like Nvidia. Having stated that, they will present helpful perception into potential market disparities.

So, what’s the newest on this entrance for Nvidia? Primarily based on 52 analysts protecting the inventory, the common 12-month value goal is $175. That’s round 26% larger than the present share value of $138.

Valuation

Lastly, now we have the valuation. Primarily based on present FY26 estimates, the inventory is buying and selling at roughly 31 occasions ahead earnings. That doesn’t look too demanding to me, given the corporate’s speedy development.

Combining this with the $175 value goal, a convincing case might be made that it is a development inventory to contemplate shopping for.

What might go fallacious?

Nonetheless, as Stanford laptop scientist Roy Amara as soon as stated: “We are likely to overestimate the impact of a expertise within the brief run and underestimate the impact in the long term.”

In different phrases, transformative new applied sciences have not often averted early speculative bubbles all through historical past. The web was essentially the most well-known instance, although there have been others.

Furthermore, round 36% of Nvidia’s gross sales got here from simply three clients within the final quarter. If these clients cut back their AI infrastructure spending after preliminary build-outs, the chipmaker might expertise a direct slowdown in income development.

Given this medium-term uncertainty, I’m not going to purchase the inventory at as we speak’s value.

{kind=link}