HIVE Digital plans to develop its hash price 4x by September 2025, doubtlessly putting it among the many prime 10 public Bitcoin miners by measurement. Concurrently, it has $100M ARR goal for HPC. Is that this small-cap miner an missed alternative?

HIVE Digital Units Sights on Growth and HPC Income

The next visitor publish comes from Bitcoinminingstock.io, the one-stop hub for all issues bitcoin mining shares, academic instruments, and trade insights. Initially printed on Feb. 27, 2025, it was penned by Bitcoinminingstock.io creator Cindy Feng.

For a very long time, Bitcoin mining’s largest names get all the eye—however what about smaller ones? This 12 months, I’m launching a brand new sequence to highlight small-cap miners that always fly beneath the radar. A few of these firms have the potential to rise as future stars, whereas others might wrestle to outlive. Understanding them now may help uncover hidden alternatives or study invaluable classes. On this sequence, I’ll break down their enterprise fundamentals, financials, strategic route, and market positioning—supplying you with a transparent, unfiltered view of their strengths, weaknesses, and funding potential.

First up: Hive Digital Applied sciences, a multi-listed Bitcoin miner with publicity to each mining and Excessive-Efficiency Computing (HPC).

Firm Overview

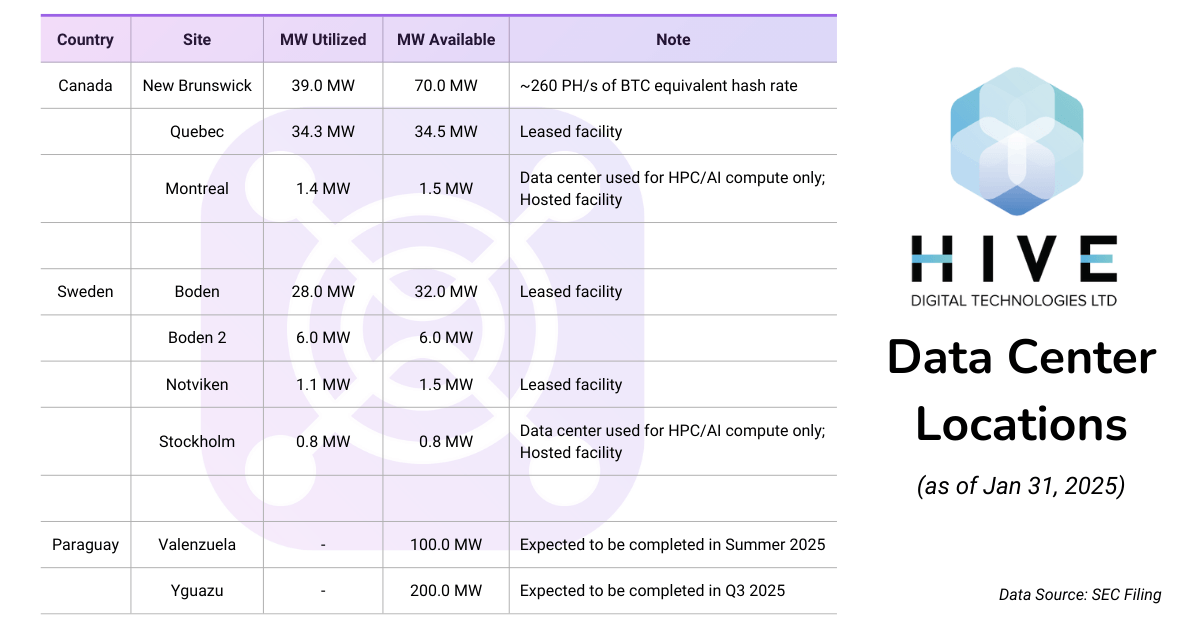

Hive Digital Applied sciences (TSX.V: HIVE; NASDAQ: HIVE ) is a publicly traded information middle operator that focuses on digital asset mining and HPC. In December 2024, it introduced the relocation of its head workplace to San Antonio, Texas, USA. The corporate has information facilities throughout a number of geographies, together with Canada, Sweden, and shortly Paraguay. It’s identified for its dedication to inexperienced vitality, primarily using hydroelectric and geothermal to energy its operations.

Enterprise Arms

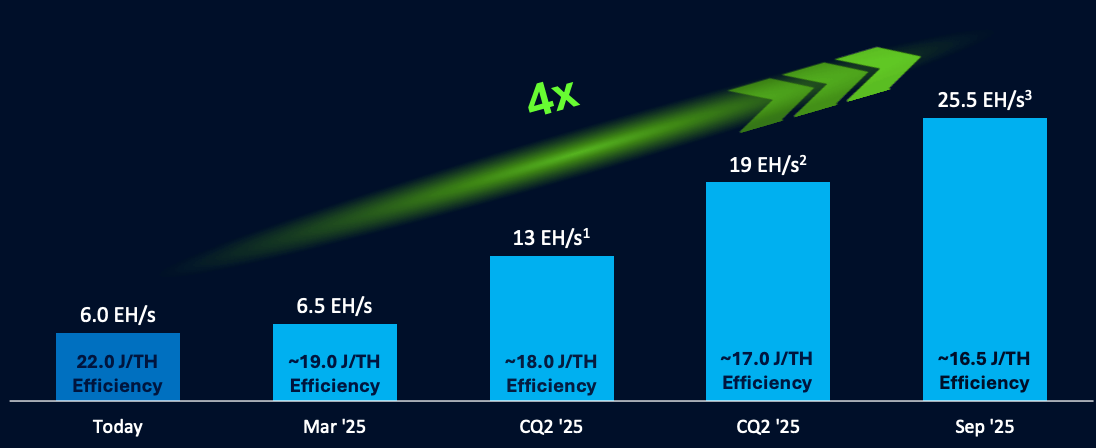

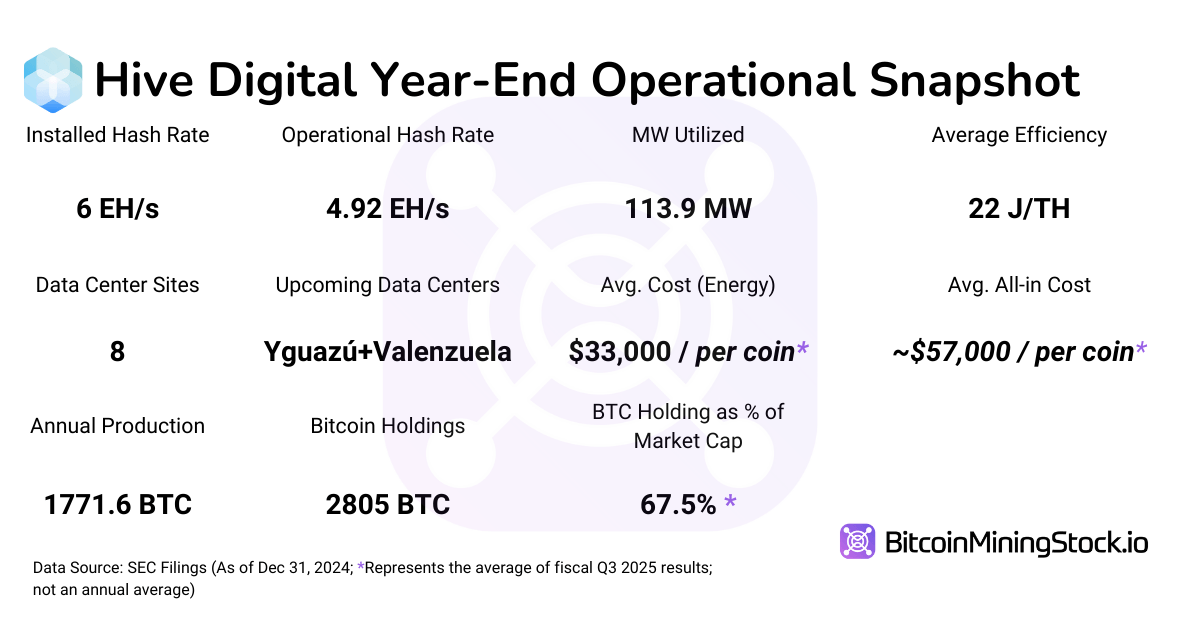

- Mining Operations: The corporate operates a complete hashrate of 6 EH/s (as of Jan 31, 2025), with an aggressive enlargement plan to achieve 25 EH/s by September 2025.

HIVE plans for 4x hash price development by September 2025 (screenshot from the corporate presentation)

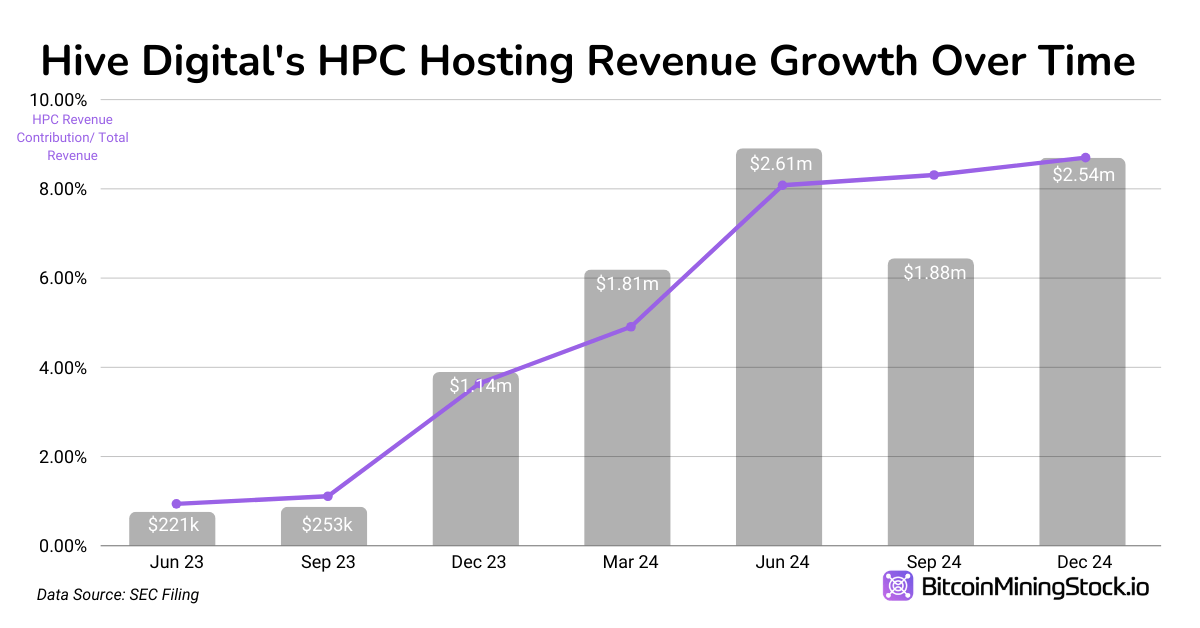

- HPC & AI Computing: HIVE was among the many first public miners to pivot to HPC, leveraging its GPU-based Ethereum mining experience. As early as 2023, the corporate reported $1.61 million in income from HPC internet hosting. Right this moment, Hive continues to make the most of its current information facilities in Montreal (Canada) and Stockholm (Sweden) for HPC providers. Moreover, the corporate plans to supply GPU server leases via market aggregators and discover a brand new cloud service providing.

Monetary Highlights: Income Decline and Profitability Enchancment

Notes: HIVE presents monetary comparisons throughout totally different intervals in its newest report. The revenue assertion follows a typical year-over-year comparability (Dec 31, 2024, vs. Dec 31, 2023), whereas the steadiness sheet is in comparison with March 31, 2024. In the meantime, the money stream assertion makes use of a nine-month comparability (Dec 31, 2024, vs. Dec 31, 2023). To make sure consistency and facilitate significant evaluation, this report primarily focuses on year-over-year comparisons the place accessible.

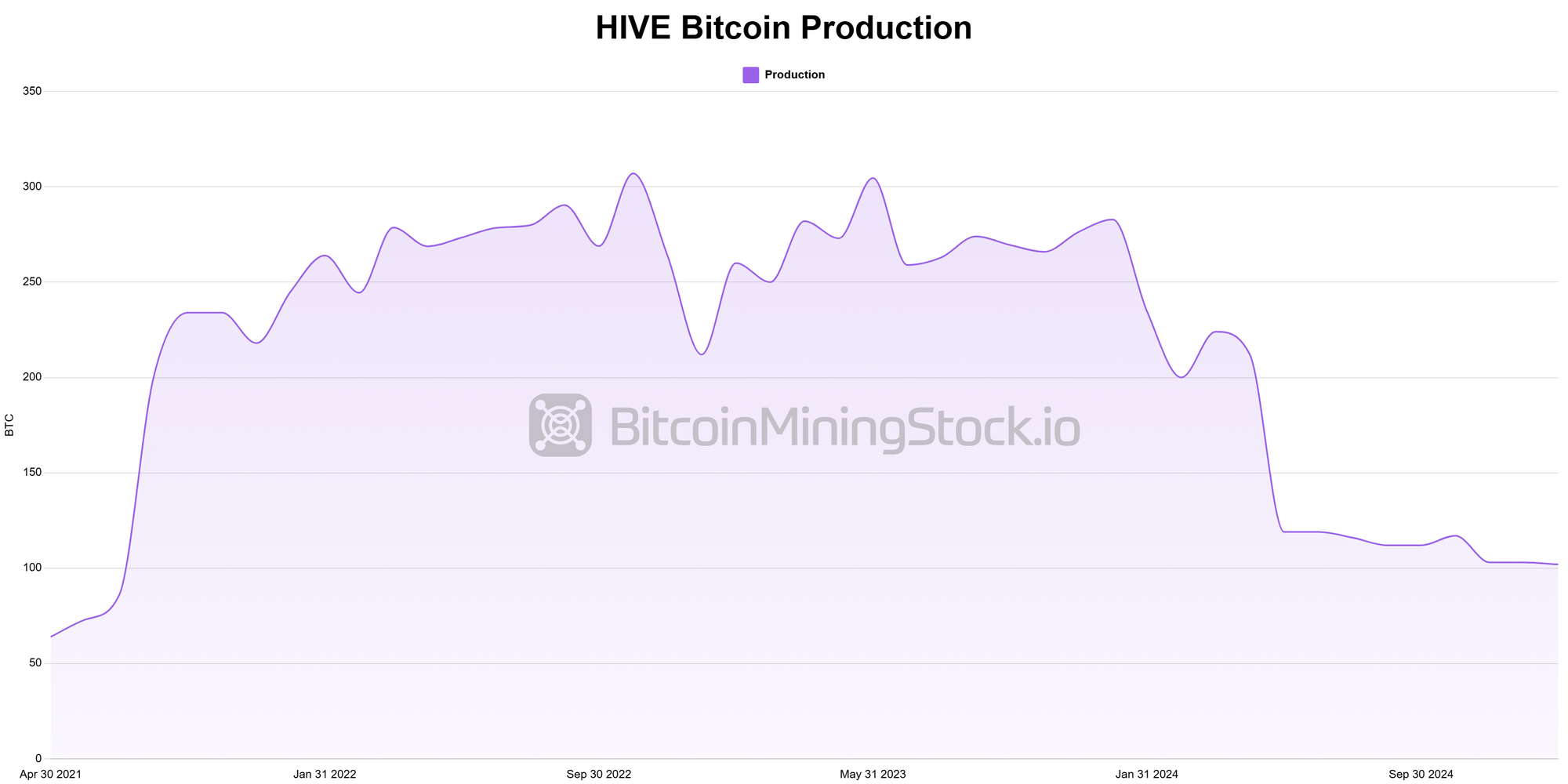

HIVE Digital Applied sciences’ fiscal Q3 2025 (Oct 1 – Dec 31, 2024) noticed a decline in income in comparison with earlier 12 months. The first issue of decline is much less BTC manufacturing as a result of Bitcoin halving occasion in April 2024. Nevertheless, the corporate has a big turnaround with internet revenue ($1.27 million vs -$6.95 million), benefiting from Bitcoin value appreciation, rising HPC enterprise and value optimizations.

Key Revenue Assertion Metrics

- Income: $29.2 million (-6.5% YoY) vs. $31.3 million in Q3 2024. This decline was pushed by a drop in Bitcoin mining income (-11.3% YoY) resulting from decrease manufacturing (322 BTC vs. 830 BTC in Q3 2024), following the April 2024 Bitcoin halving. Nevertheless, Bitcoin value appreciation and powerful HPC income development (+123.6% YoY, reaching $2.5M) helped offset the decline.

- Adjusted EBITDA: $17.3 million (vs. $17.4M in Q3 2024).

- Web Revenue: $1.3 million (vs. a $7.0 million internet loss in Q3 2024). The swing to profitability was pushed by a $6.9M achieve on asset gross sales, $5.7M international alternate achieve, and improved price efficiencies, regardless of a decrease gross margin in comparison with the earlier 12 months.

- Gross Margin: 21% (vs. 36% in Q3 2024), impacted by a sharp rise in community problem (99.9T vs. 64.1T YoY) and greater vitality prices, notably in Sweden, the place tax coverage adjustments led to elevated electrical energy bills.

- Bitcoin Manufacturing: 322 BTC (-61% YoY) vs. 830 BTC in Q3 2024. The Bitcoin halving occasion decreased mining rewards, regardless of enhancements in HIVE’s total hashrate and effectivity.

Historic information of public Bitcoin miners is now accessible on Bitcoinminingstock.io.

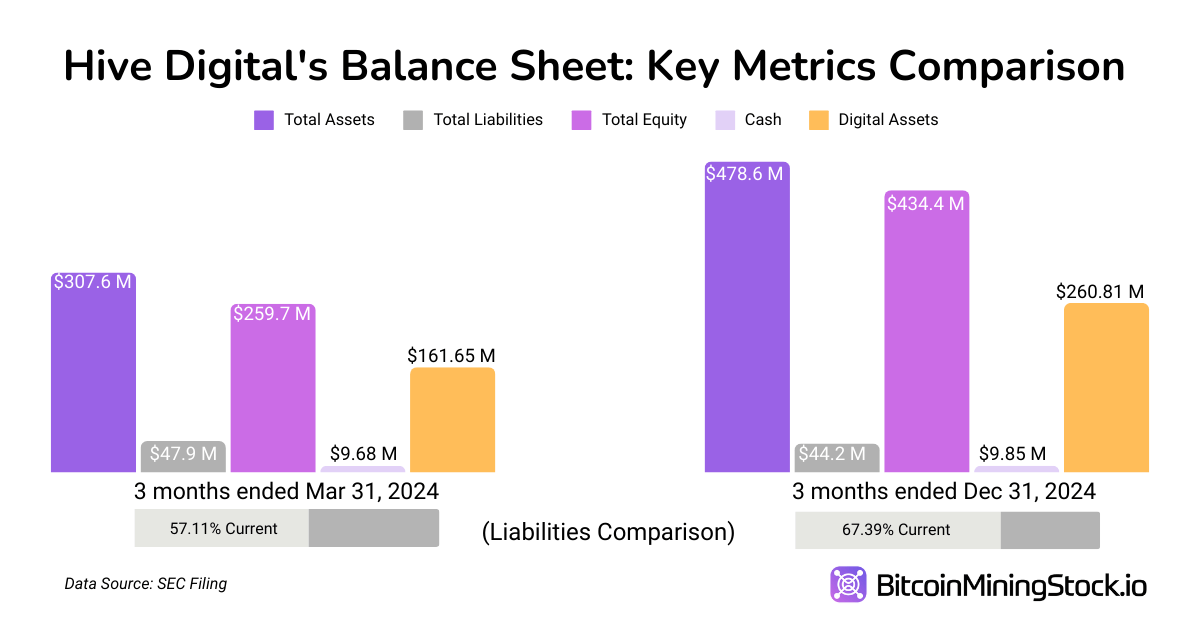

Key Steadiness Sheet Metrics (Three months ended December 31, 2024, vs. Three months ended March 31, 2024 )

- Whole Belongings: $478.6 million (+55.6%) vs. $307.6 million. The rise was pushed by greater Bitcoin holdings (2,805 BTC) and ongoing investments in mining infrastructure, notably fleet upgrades and new information middle expansions in Paraguay.

- Whole Present Liabilities: $29.8 million (+8.8% ) vs. $27.4 million. The rise displays greater short-term obligations linked to infrastructure investments.

- Lengthy-term Liabilities: $14.4 million (-29.8%) vs. $20.5 million. The lower is attributed to ongoing debt repayments, bettering HIVE’s monetary stability whereas sustaining ample liquidity for enlargement.

- Stockholders’ Fairness: $434.4 million (+67.3%) vs. $259.7 million. Progress in fairness was fueled by profitable fairness choices, greater asset valuations, and retained earnings.

- D/E Ratio: 0.10 (vs. 0.18 ). The corporate maintained a really low leverage, utilizing fairness raises relatively than debt to fund enlargement.

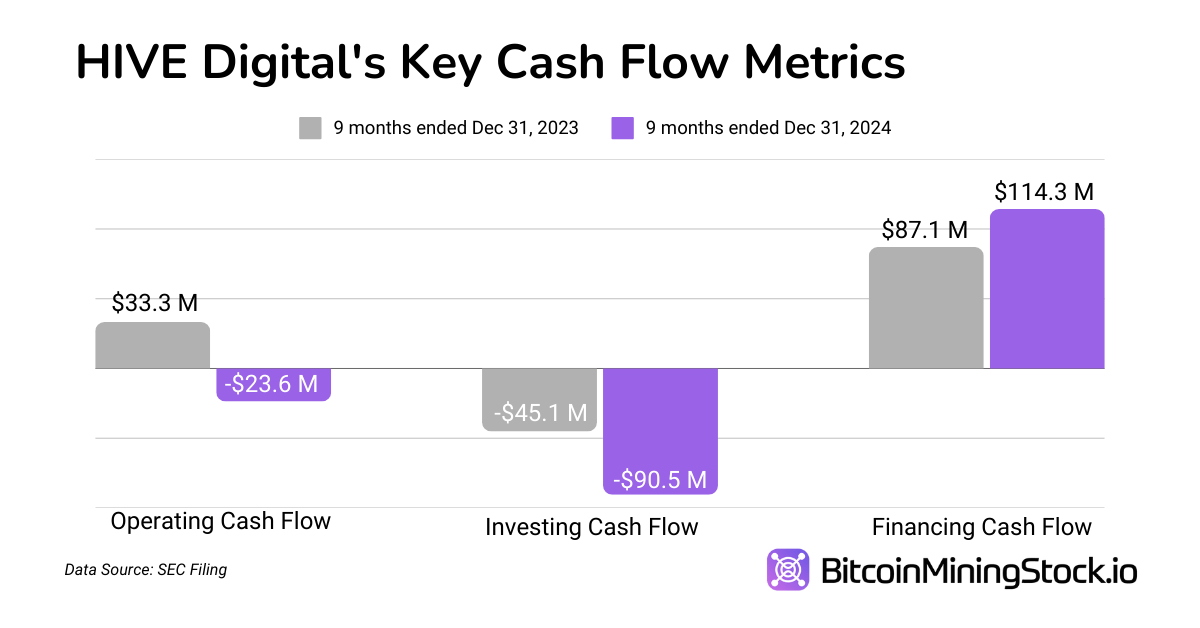

Key Money Movement Metrics (9 months ended Dec 31, 2024, vs. 9 months ended Dec 31, 2023)

- Working Money Movement: $23.6 million outflow (vs. $33.3M influx). This shift to destructive working money stream was resulting from decrease BTC gross sales quantity and better working capital wants, as the corporate HODL’d Bitcoin relatively than promoting at decrease costs.

- Investing Money Movement: $90.5 million outflow (vs. -$45.1 million). HIVE doubled capital investments, allocating $59.6M for brand spanking new mining gear and buying the Boden 2 information middle in Sweden, as a part of its long-term enlargement technique.

- Financing Money Movement: $114.3 million influx (vs. $87.1M). HIVE raised $121.0M via fairness choices, whereas repaying $3.0M in loans, sustaining a robust money place for upcoming infrastructure.

Foremost Valuation Metrics

Hive’s market cap at the moment stands at $385.4 million (Advertising closing on Dec 31, 2024). To higher perceive its valuation, we examine it towards key monetary metrics:

- Enterprise Worth (EV): $158.97 million (Market Cap + Debt – Money & Bitcoin Holdings). Hive trades at an EV per BTC mined of $89,834, near BTC’s market value. If Hive efficiently executes its enlargement and HPC technique, its present undervaluation presents a possible re-rating alternative.

- EV/EBITDA Ratio: 7.6x ($158.97M / $20.7M)

- Shares Excellent: 140.20M (+32%)

- EPS: $0.00988 (bettering from earlier −$0.0788)

- P/S Ratio: 13.2x ($385.4M / $29.2M)

- BTC Holding per Market Cap: 67.5%, that means a big portion of its valuation is tied on to BTC reserves.

Operational Metrics: Hash Fee & Effectivity

Key Hash Fee & Effectivity Metrics:

- Hash Fee: 6 EH/s, with a goal of 25 EH/s by September 2025.

- Fleet Upgrades: 11,500 items of Avalon A1566 ordered in Oct and Nov 2024 (6,500 of which has been deployed by Feb 11, 2025)

- Common Effectivity: 22 J/TH, anticipated to enhance to 16.5 J/TH by September 2025.

- Direct Vitality Price Per BTC: $33,000

- Whole Price Per BTC (Together with Depreciation & Financing): ~$57,000

Key Digital Belongings Holding & Gross sales Information:

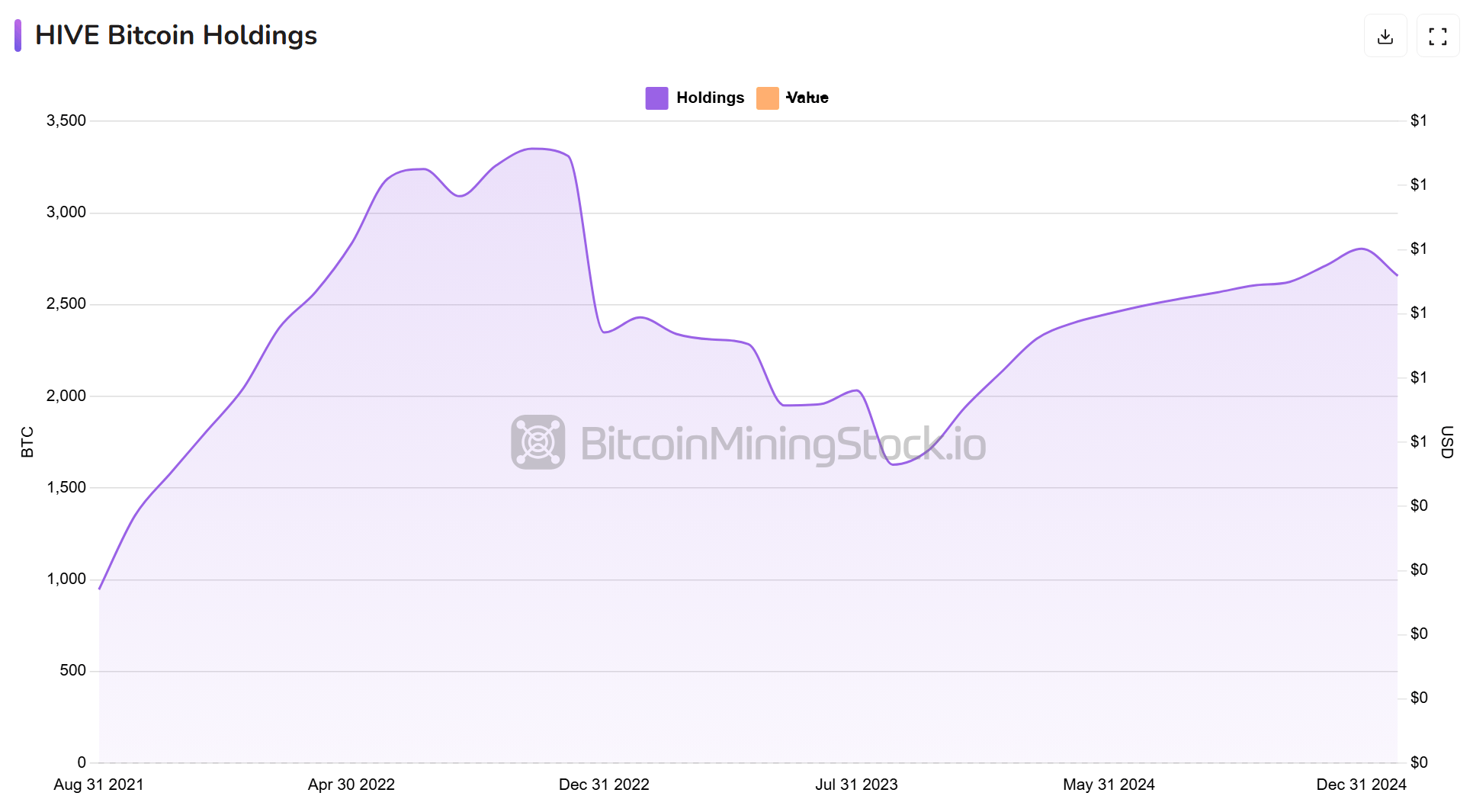

- Whole Bitcoin Held: 2,805 BTC (unencumbered, mined with clear vitality).

- BTC Offered Through the Quarter: ~$8.4M vs. ~$30.7M in 2023

- Funding Operations: Fairness financing of $121M as an alternative of extreme BTC gross sales.

- Cash are saved with Fireblocks Inc., not on exchanges

- No pledge or staking on BTC holdings

*Hive nonetheless holds $371k value of different cash (ETC+ others)

Strategic Strikes

Bitfarms Web site Acquisition in Paraguay: The Core Progress Engine

Buying Bitfarm’s facility is “a formative step in the direction of our technique to have 25 EH/s by September.” The deal features a 200MW hydro-powered mining website (nonetheless beneath building) in Yguazú, Paraguay.Upon completion, Hive’s operational capability in Paraguay will whole 300MW, which might be one of many largest Bitcoin mining operations in Latin America.

Administration additionally has strengthened that Paraguay stays the corporate’s main focus for scaling operations. As CEO Aydin Kilic said, “We see alternatives within the U.S. resulting from a extra favorable regulatory surroundings, however our main focus stays on scaling operations in Paraguay for now.”

Growth Roadmap:

- 100MW Yguazú Section 1 (April 2025): Including 6 EH/s.

- 100MW Valenzuela (June 2025): Including 6.5 EH/s.

- 100MW Yguazú Section 2 (September 2025): Including 6.5 EH/s.

- Goal fleet effectivity: 16.5 J/TH by September 2025.

Hive Digital’s Growth Roadmap in Paraguay (screenshot from the corporate web site)

Funding in HPC & AI Infrastructure: Small however Rising

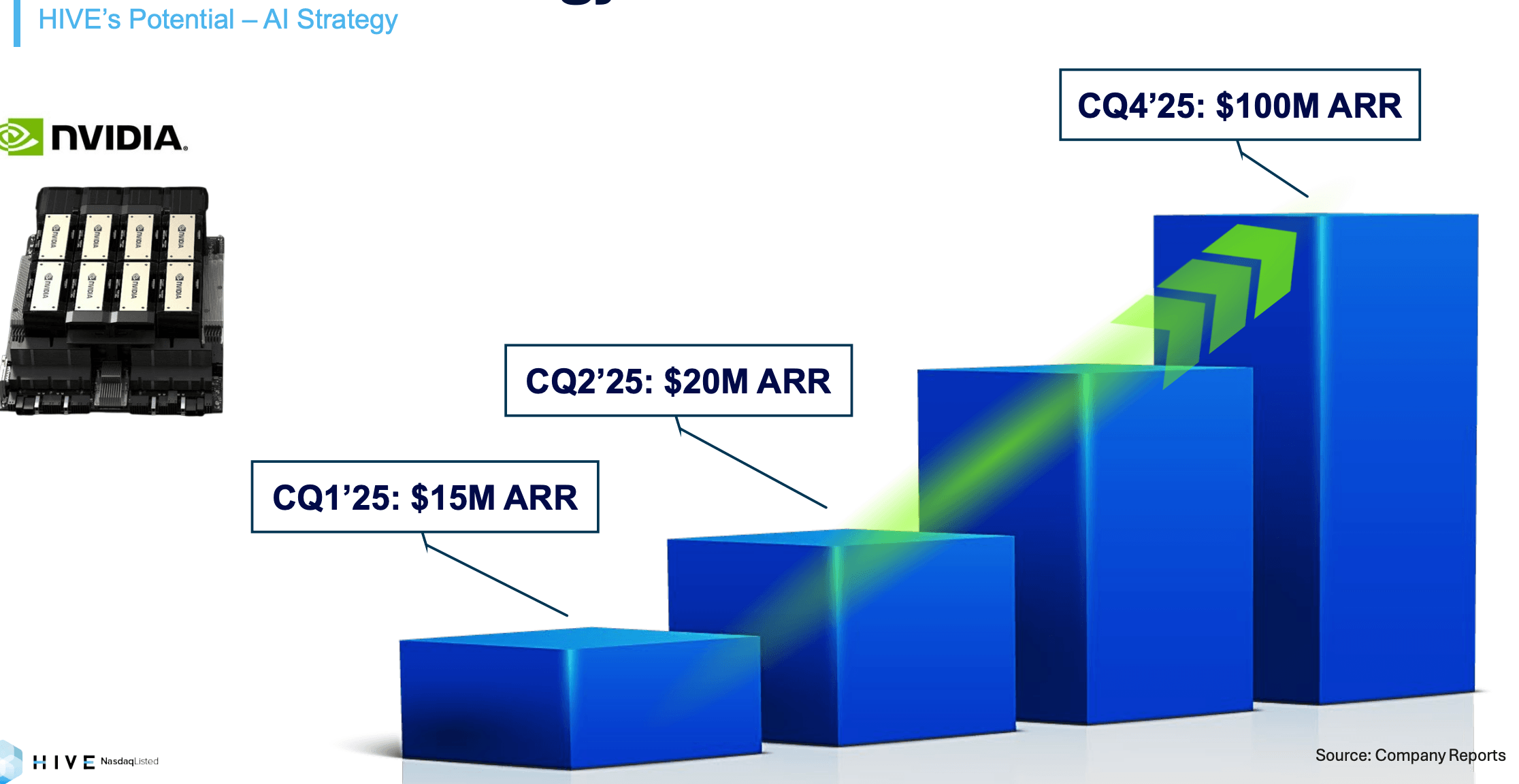

Whereas nonetheless small, AI/HPC income is rising quickly. Hive reached $2.5 million income in fiscal Q3 2025 (up 124% YoY) from its HPC operations, and the corporate initiatives to achieve $20 million subsequent quarter and $100 million annualized income by the tip of 2025.

Hive’s HPC/AI Income Progress Projection (screenshot from the corporate presentation)

Present infrastructure:

- 4,000 GPUs in use (together with NVIDIA A4000, A5000, A40, and H100 )

- 508 Nvidia H200 GPUs anticipated by Q1 2025 (add $9 million in top-line income as soon as deployed)

- In preparation to place themselves for next-generation liquid-cooled Nvidia Blackwell GPUs

- Nvidia Cloud Associate standing secured, bettering credibility.

In contrast to friends who concentrate on partnerships with hyperscalers, Hive plans to hire on to end-users for LLM computations via on-demand market aggregators, along with providing HPC internet hosting. This enterprise phase continues to develop and increase.

Different Notable Modifications:

- Head workplace relocation to San Antonio, Texas. In response to Frank Holmes, the Government Chairman, “HIVE feels safer working within the U.S., given the shift in authorities help towards Bitcoin mining, blockchain networks, and self-custody of digital belongings.”

- Transitioning to the U.S. GAAP reporting in fiscal year-end March thirty first to enhance transparency and comparability with different Bitcoin miners.” Personally I actually like this transfer as it’s going to assist standardize monetary reporting and make cross-company evaluation extra dependable.

For instance, HIVE’s newest investor presentation highlights “best-in-class ROIC” and the “lowest company G&A,” however my guide calculations yield totally different outcomes. The primary distinction is that HIVE makes use of adjusted non-IFRS metrics, excluding prices reminiscent of depreciation, stock-based compensation, and Bitcoin honest worth changes, which might current a extra favorable monetary image.

To make sure goal comparisons, this report excludes such metrics and focuses on standardized monetary information. The transition to GAAP ought to improve readability for buyers assessing HIVE towards its trade friends.

Remaining Ideas

Hive presents a dynamic mix of bitcoin mining and HPC providers, positioning it for each substantial development and inevitable volatility. From a steadiness sheet perspective, the corporate stays financially conservative with a low D/E ratio, however it does rely closely on fairness raises to fund its capital-intensive enlargement plan (4x by September 2025). Its growth in Paraguay may considerably improve mining capability and place it among the many prime 10 public miners by way of measurement, enhancing its trade visibility. Mixed with the shift to U.S. GAAP reporting and the relocation of headquarters to Texas, this transition might assist entice buyers searching for regulatory readability and transparency.

HIVE’s Bitcoin mining enterprise presents each strengths and challenges. The corporate at the moment advantages from a decrease common Bitcoin manufacturing price, even compared to CleanSpark, one of the vital environment friendly miners. With improved fleet effectivity, better scale, and entry to decrease electrical energy prices in Paraguay, its mining operations may grow to be extra aggressive throughout the trade. Nevertheless, the growth of its Paraguay websites is topic to potential delays from unexpected circumstances, and Bitcoin’s value stays extremely risky. Given its present low gross margin, any downturn in Bitcoin’s value may put vital strain on profitability.

On the identical time, HIVE’s HPC enterprise, although nonetheless a small contributor, is gaining traction and has the potential to grow to be a significant income driver. The corporate is actively increasing this phase by introducing new cloud service choices and scaling its AI computing operations. If HIVE efficiently attracts high-value AI prospects and reaches its purpose of $100 million in annualized income by the tip of 2025, its HPC enterprise may present a secure, high-margin income stream, serving to to offset the volatility of Bitcoin mining. Nevertheless, this goal is very formidable, as the corporate generated solely $8.84 million from HPC in 2024, that means it could have to develop practically 10x inside a 12 months.

For buyers with a excessive tolerance for danger—notably these optimistic about long-term Bitcoin value traits and the evolving AI ecosystem—HIVE could also be a pretty high-risk, high-reward speculative alternative. Nevertheless, its success will depend upon the Bitcoin value, the efficient execution of its enlargement plans in Paraguay, and the development of its HPC enterprise. Traders ought to intently monitor these elements, as they are going to be essential in figuring out HIVE’s future efficiency.

{kind=link}