Picture supply: Getty Pictures

The earliest an funding journey begins, the higher. If a 30-year-old started making month-to-month contributions of some hundred kilos in a Shares and Shares ISA immediately, they may — by the point they hit State Pension retirement age — probably get a seat on millionaire’s row.

That is because of the mathematical miracle of compounding. Making a return on previous returns can, over many years, lead to transformational wealth.

Let me present you ways.

Sage phrases

Investing in shares, belief and funds is usually a bumpy experience. As we’ve seen in current days, inventory markets can sharply reverse relying on geopolitical and maroeconomic situations.

On this case, share costs have dropped amid fears of growth-crushing commerce tariffs between the US and its main buying and selling companions, and the potential impression of those import taxes in fuelling inflation.

But it’s additionally essential to keep in mind that, over the long run, share costs are inclined to get better and develop, rewarding affected person traders who keep the course.

I’m reminded of billionaire investor Warren Buffett‘s smart phrases on the inventory market’s exceptional bouncebackability. The so-called ‘Sage of Omaha’ as soon as identified that:

Within the twentieth century, the USA endured two world wars and different traumatic and costly navy conflicts; the Despair; a dozen or so recessions and monetary panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. But the Dow rose from 66 to 11,497.

As we speak, the Dow Jones sits round 41,453 factors.

A £1.6m pension pot

It is a good instance of how investing with a long-term strategy can repay.

Since its inception in 1957, the S&P 500 has additionally delivered mighty shareholder income. Its common annual return is a formidable 10.2%. If this continues, a 30-year-old often investing within the index in a Shares and Shares ISA might construct a life-changing retirement fund.

Let’s say they make investments £300 every month between now and their State Pension age of 68. Due to the wealth-building energy of compounding — and the tax-saving qualities of the ISA — they’d have generated a whopping £1,639,317 to retire on (excluding dealer charges).

Keep in mind although, that 10.2% return I’ve described isn’t assured.

Taking the easy route

By making a diversified portfolio, our investor might stand a significantly better probability of retiring with a considerable nestegg. Buying shares throughout quite a lot of industries, sub-sectors and geographies may help them mitigate threat and capitalise on many various funding alternatives.

To focus on that 10.2% common annual return merely, our 30-year-old might select to purchase an exchange-traded fund (ETF) that tracks the efficiency of the S&P. The HSBC S&P 500 (LSE:HSPX) is the one I maintain in my very own portfolio.

With its ongoing cost of 0.09%, it’s one of the crucial cost-effective index-tracking funds on the market.

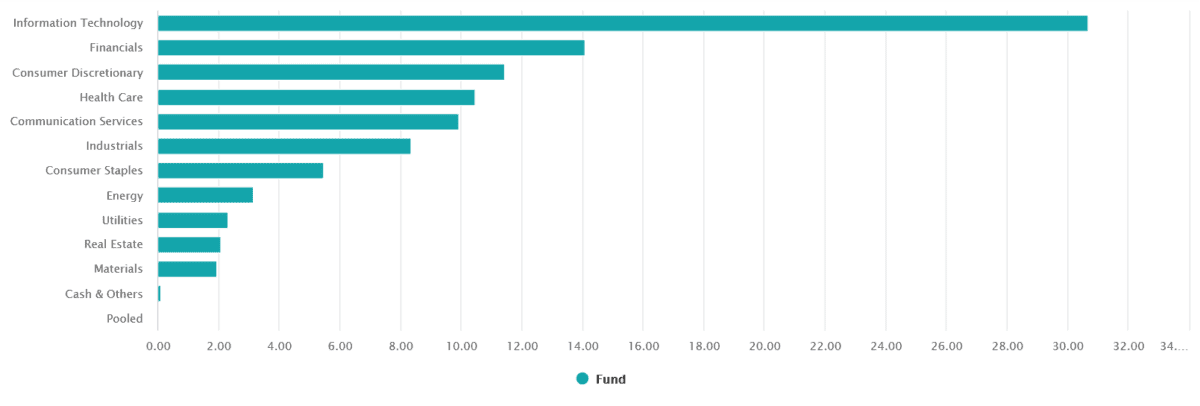

As you possibly can see from the breakdown, the fund permits traders to successfully diversify throughout a spread of sectors. And with tech shares like Nvidia, Microsoft and Apple making up a big portion of the fund, it additionally has vital long-term progress potential because the digital revolution rolls on.

The fund might face headwinds if sentiment in the direction of US shares as a complete weakens. However general, I feel it’s an amazing one to think about as a method for traders to intention for a big retirement pot.

{kind=link}