Picture supply: Getty Pictures

The Self-Invested Private Pension (SIPP) is — just like the Particular person Financial savings Account (ISA) — an efficient product for constructing a pot of money for retirement.

Like a Shares and Shares ISA, any capital beneficial properties or dividend earnings generated in a SIPP are shielded from the taxman. This offers buyers with extra capital, and subsequently the means for superior exponential progress via compounding.

However that’s not all. With tax aid, SIPP buyers additionally get tax aid from the federal government with which to develop their portfolio.

Right here’s how even a 40-year-old with no financial savings or investments may probably construct a big retirement fund with a £500 month-to-month contribution.

Please notice that tax therapy will depend on the person circumstances of every consumer and could also be topic to vary in future. The content material on this article is supplied for info functions solely. It’s not supposed to be, neither does it represent, any type of tax recommendation. Readers are chargeable for finishing up their very own due diligence and for acquiring skilled recommendation earlier than making any funding selections.

Tasty tax aid

That £500 funding may not appear to be loads at first look. At £6,000 a yr, that is effectively beneath the present annual allowance on SIPPs. Usually, that is both £60,000 or a sum equal to a yearly earnings, whichever’s decrease.

However because of beneficiant tax aid, the precise worth of those contributions may be significantly larger.

Reduction is ready on the following charges:

- 20% for basic-rate taxpayers

- 40% for higher-rate taxpayers

- 45% for additional-rate taxpayers

So in impact, a basic-rate taxpayer is placing £625 into their SIPP every month by investing £500 of their very own money.

Greater-rate and additional-rate taxpayers get pleasure from the identical £125 month-to-month top-up straight into their pension. The rest is claimed again by way of self-assessment.

Investing correctly

A boosted month-to-month contribution is a big perk for SIPP customers. However as with all different monetary product, the quantity of wealth generated in the end will depend on the best way they use their cash.

Buyers should purchase all kinds of shares, trusts and funds with a SIPP. Or they will merely select to carry their cash in money.

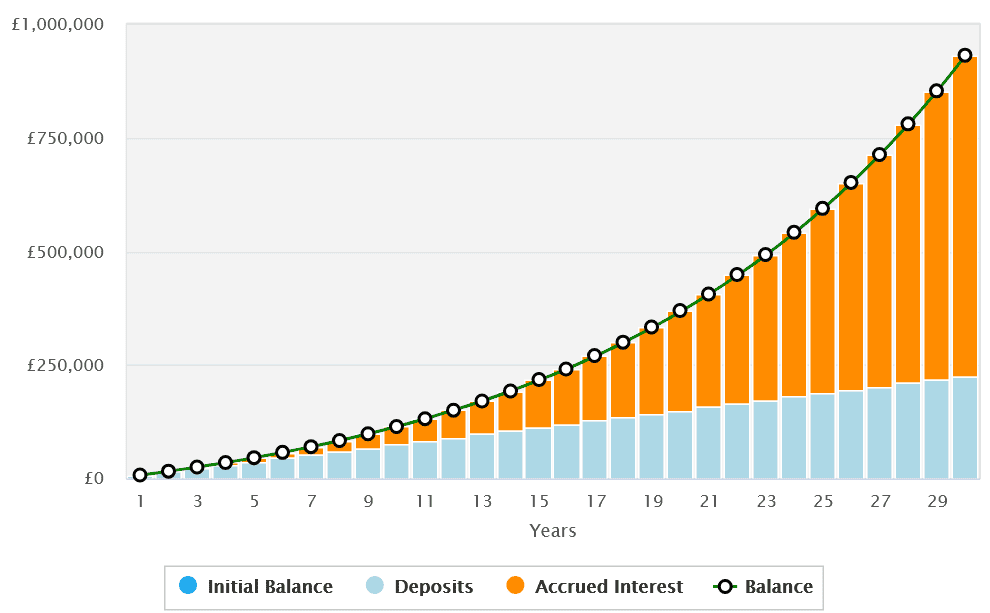

The distinction on long-term returns may be appreciable. Let’s say a basic-rate taxpayer was to get a median 3.5% financial savings price on their money steadiness. Based mostly on a £625 month-to-month contribution they might, after 30 years, have a pension price roughly £397,133.

Now let’s say they as an alternative bought shares that supplied a median annual return of 8%. With the identical contribution over three a long time they’d be sitting on a considerably larger sum of £931,475.

Getting began

There’s no proper and mistaken approach to method SIPP investing. Your best option for every of us relies on our private funding targets and tolerance of threat.

However I imagine these looking for to supercharge their retirement fund ought to take into account investing in shares. Investing in a fund or a belief can scale back threat too by spreading capital throughout a basket of property.

The F&C Funding Belief‘s (LSE:FCIT) an asset that ticks lots of bins for me and could possibly be price additional analysis. Courting again to 1868, it has an extended and distinguished report of delivering wholesome returns, together with 53 consecutive years of dividend progress.

Right now, it holds shares in additional than 400 totally different international corporations unfold throughout a number of sectors. Main names embody chipmaker Nvidia , monetary providers supplier Mastercard, drugmaker Eli Lilly and retailer Costco.

This diversification doesn’t defend buyers from disappointing returns throughout downturns. However over the long run it’s confirmed an efficient manner of balancing threat administration and optimising returns.

Since January 2015, the F&C Funding Belief’s supplied a median annual return of 11.4%. If this continues (and that’s an enormous ‘if’ because it’s not assured), contemplating a £625 month-to-month funding right here may assist buyers construct a big SIPP loads prior to 30 years.

{kind=link}