Picture supply: Getty Photos.

People can attempt to construct a wholesome second earnings for retirement in plenty of methods. Merchandise just like the Money ISA have loved a renaissance extra not too long ago as financial savings charges have perked up.

In line with HM Income and Customs, the variety of Money ISAs that have been subscribed to in 2022/23 rose by a whopping 722,000 yr on yr, to only beneath 7.9m. It’s no coincidence that this coincided with the Financial institution of England beginning its rate of interest climbing cycle in late 2021.

Nonetheless, opting to only save money reasonably than make investments might end in vital missed returns, and the scenario could solely worsen over time.

Let me present you ways.

Charges to drop?

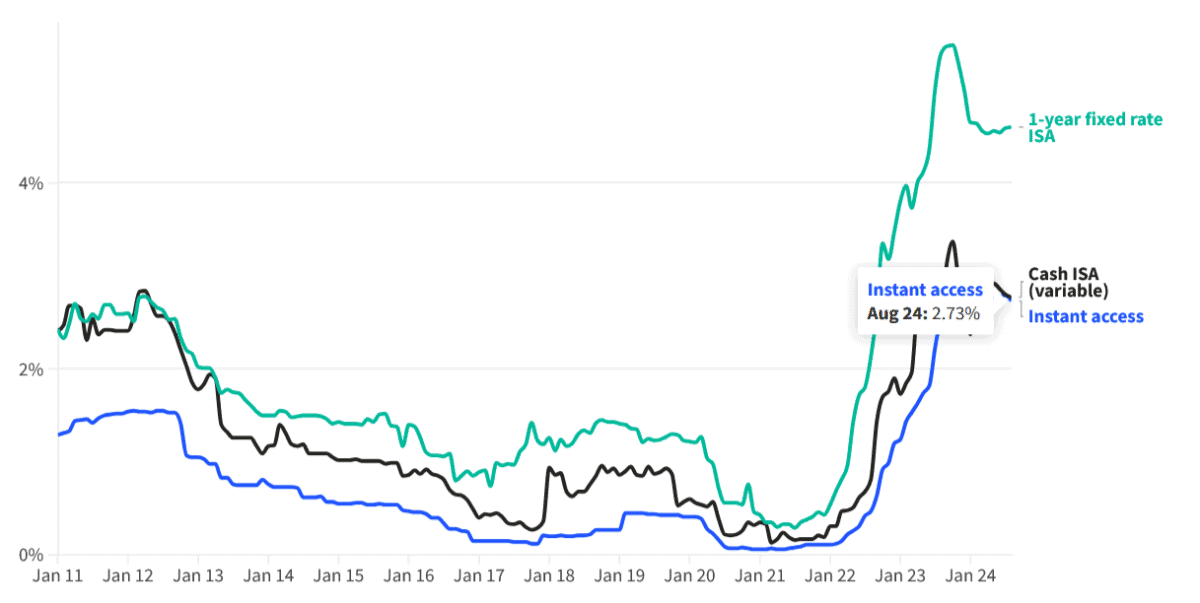

Immediately, among the best easy-access Money ISA available on the market gives a wholesome 5.12% rate of interest. Because the chart under exhibits, the common charge for these tax-friendly merchandise is comfortably forward of what savers loved between 2011 and 2022.

Nonetheless, charges are tipped to fall steadily throughout the market because the BoE begins to loosen financial coverage. So leaving all one’s cash locked in a financial savings account might be a large mistake.

For the sake of this instance, let’s say that the best-paying Money ISA gives a charge of 4% for the following 30 years. A £300 funding every month at this charge would make me £208,215 over the interval.

If I then drew down 4% of this annually, I’d have a month-to-month earnings of £694.

Higher returns

That’s far under what I might be making if I invested in, say, the FTSE 100 or FTSE 250 as a substitute. These UK share indexes have offered a mean long-term return of seven% and 11% respectively over the long run.

Nonetheless, it’s important to do not forget that previous efficiency isn’t a dependable information to future returns. Share investing is far riskier than parking my cash in a safe financial savings account, and I might even make a loss on sure shares. This is the reason having a certain quantity in financial savings for emergencies is at all times a good suggestion.

Lowering threat

That is additionally why investing in an exchange-traded fund (ETF) might be a good suggestion. These monetary devices unfold threat by allocating my money throughout a variety of equities.

Based mostly on the above, shopping for the iShares FTSE 250 UCITS ETF (LSE:MIDD) might be a fantastic thought. By investing my money throughout lots of of various corporations, I’ve publicity to a large number of industries and geographies, thereby minimising the impression of underperformance in anybody explicit space.

Moreover, the ETF offers me with a mixture of cyclical and defensive shares, which may present me with a easy return over time. There’s the danger, nonetheless, that the fund’s deal with UK shares might be an issue ought to broader demand for British property decline.

If the FTSE 250’s long-term return of 11% continues, a £300 month-to-month funding on this ETF would flip into £841,356 after 30 years, excluding the impression of slight monitoring errors.

That may then make me a month-to-month £2,805 passive earnings based mostly on a 4% drawdown charge. That’s 4 occasions larger than the £694 I’d get pleasure from by spend money on that 4%-yielding Money ISA talked about above.

It’s why I plan to proceed investing in shares and funds over merely saving money.

{kind=link}