Picture supply: Getty Photographs

Hostelworld (LSE: HSW) is a small-cap UK inventory that suffered through the pandemic 5 years in the past. As international journey got here to a standstill, the hostel-booking platform’s income fell off a cliff, driving the agency into the pink.

Nevertheless, with these darkish Covid days fortunately within the rear-view mirror, the share value has been steadily regaining misplaced floor. It’s gone from 77p again then to 136p, representing a achieve of roughly 79%.

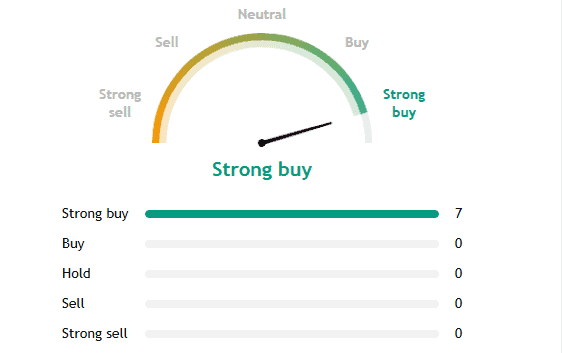

But Metropolis brokers see additional potential positive aspects forward, and have a consensus value goal of 192p. That’s 40% greater than the present stage, although there’s no assure it can attain that value inside the subsequent 12 months.

Apparently although, all seven analysts overlaying this small-cap inventory are very bullish, score it as a Sturdy Purchase.

What do they see in Hostelworld? Let’s try some particulars.

Area of interest market

For these unfamiliar, Hostelworld is principally the Airbnb of hostels. It acts as a market, taking fee when travellers e book lodging by way of its web site or app.

The corporate has hostel companions in over 180 international locations, and youthful travellers make up nearly all of bookings. In 2019, Hostelworld generated €80.7m in income and a web revenue of €8.4m. Then it endured three years of losses earlier than returning to profitability in 2023 as international journey rebounded after the pandemic.

In 2025, it’s anticipated to report €97.5m in income and a web revenue of €13.9m. So it’s managed to climate the Covid storm, and is rising as soon as once more.

Development plan

Constructing on this momentum, administration not too long ago set out a progress plan. The goal is for low double-digit income progress in 2026 and 2027, with an adjusted EBITDA margin above 20%, and adjusted free money move conversion of about 70%.

The corporate has a robust stability sheet, with no debt, and an €8m web money place on the finish of 2024. The dividend has been reinstated, with a progressive coverage of 20%-40% of adjusted post-tax revenue, beginning within the second half of this 12 months.

It has additionally simply commenced a £5m share buyback programme.

Social community

One space the agency is seeing success in is its social community. This permits members to message, join, and meet up with like-minded travellers.

Launched in Q2 of 2022, the community had 2.6m members by Q1 2025. These social members are reserving 2.2 occasions greater than non-members over the primary 91 days after signing up. So there may be proof of robust community results rising right here.

Hostelworld can even begin together with extra funds inns and different lodging choices on its platform. Whereas which may spur progress, it additionally takes it additional into competitors with Airbnb, Reserving.com, and others.

Additionally, international journey demand may all the time be impacted by one other pandemic or some kind of international battle. So these are dangers to remember.

Respectable valuation

That stated, I just like the social community angle, because it’s prone to hold customers loyal to the platform. I see a variety of monetisation potential.

Extra repeat bookings also needs to scale back advertising spend, which has already fallen from 58% as a share of income in 2022 to 46%.

Lastly, the inventory is buying and selling at simply 11 occasions subsequent 12 months’s forecast earnings. Weighing issues up, I feel Hostelworld is value contemplating for traders in search of an inexpensive small-cap inventory.

{kind=link}